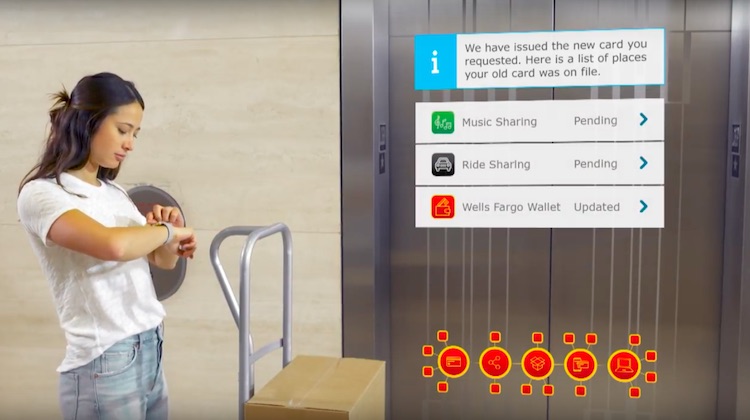

Posted on July 24, 2017July 25, 2017How Wells Fargo is letting customers take back control of their financial data

Posted on July 13, 2017July 12, 2017Adyen’s Luke Salinas: ‘The industry’s been talking about omnichannel for years’

Posted on June 14, 2017June 16, 2017Cheatsheet: What to know about Prime Reload, Amazon’s latest rewards program

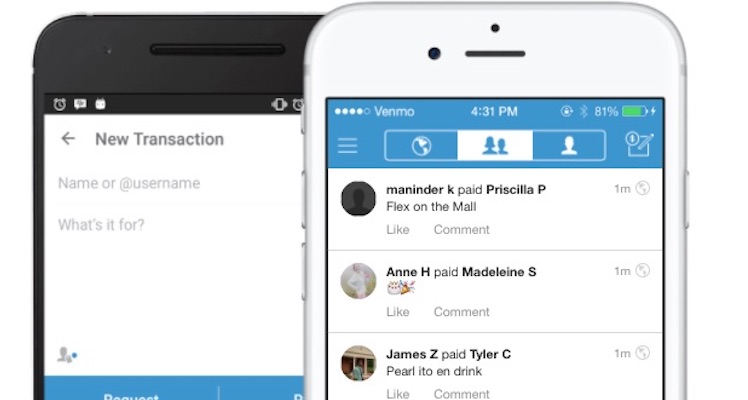

Posted on April 28, 2017April 29, 2017Venmo rising: Why PayPal wants you to pay for purchases using the app

Posted on April 13, 2017April 12, 2017CardFree’s Jon Squire: ‘It’s hard to decouple loyalty from mobile’

Posted on April 5, 2017June 9, 2017Big in Japan: How blockchain startup Ripple plans to disrupt Swift

Posted on February 10, 2017May 22, 2017How financial tech startups are reaching out to low-income Americans