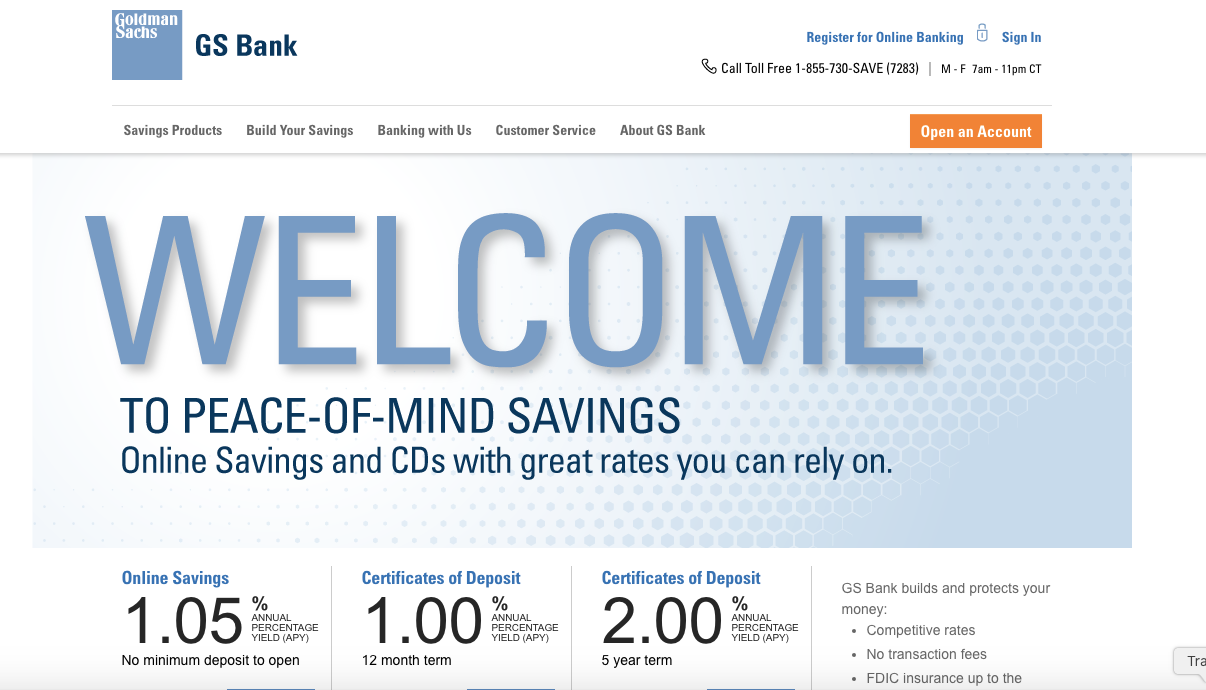

Posted on September 27, 2017September 27, 2017Goldman Sachs’ foray into consumer banking is getting aggressive

Posted on August 2, 2017August 10, 2017JPMorgan, Goldman and others are easing their dress codes in a bid for tech talent

Posted on December 21, 2016March 16, 2017Fake apologies, anti-artists, and elitist messaging: The year in financial services marketing fails