Citizens Bank hit reset on its open banking API earlier this year, modernizing the framework.

The bank began developing the new framework in 2023 under Financial Data Exchange (FDX) standards, phasing out older patchwork APIs and the risk of screen scraping. The beta arrived in mid-2024, with the full launch in Q1 2025.

The new API framework gives business, commercial, wealth, and private banking customers the same access through a single endpoint, making integration easier for fintechs and platforms with mixed user bases. The system adjusts its data output based on the account type.

In the longer term, the move positions the bank for faster collaboration with fintechs and data aggregators, creating pathways for new services to reach customers more quickly. For both businesses and individuals, this could mean smarter financial planning, more tailored products, and an improved banking experience that blends well with the tools they already use.

Oscar Gonzalez, Head of Product Management for Access & Delivery Channels at Citizens, walked me through the bank’s decision to launch its new open banking API framework and the pain points it aims to solve.

How Chime, SoFi, and Nubank are redrawing the digital banking map

For years, digital banks were the upstarts, carving out space on the promise of sleek apps, fewer fees, and a friendlier relationship with money. But the honeymoon phase of ‘fintech versus banks’ has ended. Now, the spotlight falls on who can actually scale, turn a profit, and keep growing without losing the very customers who signed up to escape Wall Street sameness.

Three names, Chime, SoFi, and Nubank, are providing three different answers to that existential question. Their recent moves echo the global digital banking sector that’s both maturing and experimenting with new endeavors.

Chime [CHYM]: The IPO debutante under pressure

Chime’s recent numbers underscore both promise and pressure. The neobank achieved profitability in the first quarter of 2025. And while the firm has seen profitable quarters before, Q1 2025 is the first to appear in tandem with its IPO filing.

By the numbers:

As of March 2025, the company reported $518.7 million in revenue for the quarter, up from $391.9 million a year earlier, with net income of $12.9 million.

For full-year 2024, revenue climbed to $1.67 billion, but the company still posted a small net loss of $25.3 million, though that’s a marked improvement from its $203 million loss in 2023.

Its member base sits at about 8.6 million active users, most of whom rely heavily on its debit and credit card products.

The fuller arc: After years of IPO speculation, Chime finally hit Wall Street this summer. Its IPO was priced at $27 a share and opened at $43, a 49% pop that resulted in a public market cap of about $9.8 billion.

The IPO raised $864 million, giving Chime a war chest to push deeper into its target market: Americans earning under $100,000 a year; nearly 200 million people who Chime argues are overcharged by the old banking system.

But IPOs are as much about what’s next as what’s past.

For banks, it’s a way to modernize without blowing up the ‘trust’ model

Coinbase, once a Silicon Valley outsider pitching crypto as an alternative to the banking system, is now doing business with the very institutions it was supposed to disrupt.

In recent weeks, two of the most prominent names in American finance — PNC and J.P. Morgan — have formally partnered with the exchange. It’s not a headline grab so much as a quiet redrawing of boundaries. The roles are shifting: banks are moving closer to the chain, and Coinbase is evolving beyond being just a crypto trading platform.

The partnerships, while distinct in purpose, point to the same broader trend: crypto is no longer relegated to the kids’ table. PNC is using Coinbase to bring crypto access directly into its digital banking experience. J.P. Morgan is embedding Coinbase integrations into consumer rewards and funding flows, and piloting tokenized deposit infrastructure on Coinbase’s Base chain.

Caught between the community banks that know every face in town and the global big ol’ boys that span continents, regional banks are increasingly making meaningful strides in marrying tradition with innovation.

In today’s 10Q edition, we spotlight two such publicly traded regional banks and the strategic moves they’re making.

Part 1: The PNC Case

A Pittsburgh-based institution with a national footprint: PNC Financial Services, headquartered in Pittsburgh, isn’t just a “regional” bank in the narrow sense. With assets of over half a trillion dollars and operations stretching from the Northeast to the Sun Belt, it occupies that increasingly blurred category of “super-regional.” It has a significant footprint in Pennsylvania, Ohio, and other Midwestern states, but its 2021 acquisition of BBVA USA widened its reach drastically into Texas, Arizona, and Alabama, giving it true coast-to-coast visibility.

PNC has positioned itself as an active player in a fast-evolving financial landscape. The bank has been steadily investing in technology, digital banking platforms, and financial literacy tools. But its most recent move signals a brave step into a territory still considered high-risk or unproven by many traditional banking peers.

Crypto, carefully – PNC’s partnership with Coinbase: In July 2025, PNC announced a partnership with Coinbase to expand access to crypto-related financial services for its clients.

Unlike many crypto service launches that flood retail markets with apps and coins, this collaboration is institutional in focus. The partnership is structured to serve institutional clients — institutional investors, businesses, high-net-worth individuals, and possibly fintech infrastructure needs — rather than the average retail investor.

The move allows PNC’s banking clients to buy, hold, and sell cryptocurrencies directly through PNC’s own platform, powered by Coinbase’s Crypto-as-a-Service (CaaS) infrastructure. This gives PNC a “plug-and-play” model for digital asset access, while maintaining the brand consistency and trust it has built over the decades.

Payoneer’s approach: embed deeply within businesses, not just alongside them

Payoneer is focusing on sustained growth. The company is increasingly integrating itself into the core operations of its users, particularly the fast-growing global SMBs and digital-first enterprises it serves.

The company’s recent product updates demonstrate its ambitions, positioning itself as a critical platform for how global businesses transfer and manage funds.

A key part of this update is Payoneer’s new integration with NetSuite. It allows for real-time data syncing between Payoneer and NetSuite’s ERP system, helping businesses cut down on manual uploads and reduce the typical end-of-month reconciliation workload.

In addition, Payoneer now supports PayPal payments globally, giving businesses another option for how they get paid. Combined with features like unified payment requests and automated invoicing, these tools are meant to ease the operational burden, particularly for smaller teams managing payments with limited resources.

The third product update enables local spending in Japanese Yen via Payoneer Card and smarter FX tools (including real-time alerts and target rate conversions). This hints at a broader strategy: helping businesses manage global money flows with the same ease they expect from domestic tools.

I had a conversation with Oren Ryngler, Payoneer’s Chief Product & Technology Officer, to learn about the motivation driving these product enhancements and how they support the company’s goal of becoming a foundational part of its clients’ financial infrastructure.

Big doesn’t mean broad for these public regional banks

It makes sense to think of American banking as a game dominated by Wall Street giants, but beneath that surface, a subtler, deeper, and less conspicuous banking layer has been steadily growing.

Across the US, regionally rooted banks have grown into billion-dollar public institutions by focusing sharply on the nuances of the communities they serve. They don’t try to be everything to everyone; their mantra is to go deep, not wide.

We take a look at five of the largest US publicly listed regional banks that have remained loyal to their geographic base, which has enabled them to establish a strong presence.

Financial institutions are drowning in payment complexity. Between legacy systems, and the accelerating pace of change in how people pay, banks face a modernization crisis that threatens their competitive position. At the FIS Emerald Conference 2025, FIS announced a partnership with Episode Six which is designed to address these challenges head-on.

Episode Six, an API-driven payments technology provider, will now be working with FIS to deliver a cloud-based, end-to-end digital payments platform. The collaboration brings together FIS’s global scale and institutional relationships with Episode Six’s modern, configurable payment infrastructure. The new partnership will allow FIs to scale beyond their local borders, without having to build new tech and processes from scratch.

“We did some pretty hefty research over an extended period of time,” said Rob Hudson, Head of International Banking, at FIS. “It became very apparent very quickly that Episode Six was the one that we wanted to work with. This was the standout opportunity for us, without doubt.”

John Mitchell, CEO and co-founder of Episode Six, emphasized the strategic nature of the partnership. “We’ve always envisioned that if we had a partner with the strengths and the scale of FIS, that our platform would be used in a much broader capacity,” he said. “This partnership is going to enable us to present a solution that will allow all of our clients to innovate at scale.”

Listen to the podcast to learn what financial executives can do to navigate legacy system constraints surprisingly well, tackle global payment complexity to expand internationally, and implement progressive modernization without putting careers on the line. It’s a conversation on practical strategies for overcoming institutional resistance to change while delivering the cloud-native solutions that modern banking demands.

Most financial institutions struggle with decades-old technology that wasn’t designed for today’s payment landscape. These systems create complexity that prevents banks from keeping pace with customer demands and fintech innovation.

“Most of the financial institutions are struggling to innovate and to keep up with the demands of their consumer and wholesale customers around real-time payments,” Mitchell explained. “You have systems that have been around for decades that are really designed for a world that’s gone – that’s changed.”

The challenge extends beyond individual institutions. Even innovative banks remain constrained by the broader payment infrastructure. “Even if a bank or a financial institution is highly innovative, forward thinking, and does wonderful stuff that other people want to copy, they’re still reliant on ancient legacy technology to move money outside of them,” Hudson noted.

This creates a cascading effect where the entire ecosystem moves slowly, regardless of individual institution capabilities. The partnership aims to break this cycle by providing modern infrastructure that can integrate with existing systems without requiring wholesale replacement.

Global complexity demands sophisticated solutions

The partnership’s value proposition centers on reducing market entry friction. Where institutions previously needed to build separate systems for each jurisdiction, the combined platform handles geographies and regulatory frameworks through a single integration. The approach transforms international expansion from a multi-year technology project into a configuration exercise.

“A lot of the customers and consumers are looking for solutions that are more global in nature,” said Chermaine Hu, CFO and co-founder of Episode Six. “The world is much more connected today than 10 to 20 years ago. So it’s getting even more complicated because you need products that can serve across different countries, currencies, and deal with different regulations.”

Hudson emphasized the regulatory complexity that the partnership helps navigate: “If you take moving money outside of the country in which you’re domiciled, things get so much more complicated.” The partnership leverages FIS’s global regulatory expertise alongside Episode Six’s flexible architecture to address these challenges systematically.

The realization that modernization is critical hasn’t hit for many

Beyond technology, the partnership faces the challenge of changing institutional mindsets around payment modernization. Many financial institutions remain hesitant to address their technology debt, either due to concerns about system fragility or reluctance to tackle complex projects.

The education that you need to do something actually [is lacking], because a lot of institutions, particularly the more technical side, are either worried about the fragility of their existing system and therefore don’t want to touch it, or they think I’ll leave that for the next guy,” Hudson explained.

This institutional inertia creates market opportunities for more agile competitors. Hudson warned that established banks face real competitive pressure: “We’ve got smaller banks already in a position where they’re taking salary deposits into their current account, and that will grow, and these big banks will start to suffer, and they’re going to have to do something.”

The partnership addresses these concerns by combining Episode Six’s modern technology with FIS’s institutional credibility. “The financial strength and the scale of FIS means so much to our organization, and it means so much to that CIO who wants to keep the lights on. That’s the trust that FIS has built over the years.” Mitchell said.

Progressive modernization over rip and replace

The industry has moved away from wholesale system replacements toward more gradual modernization approaches. This shift reflects both the practical challenges of large-scale technology overhauls and the career risks they pose to decision-makers.

“Progressive modernization has been a big idea,” Mitchell said. “In the late 2010s we saw a lot of initiatives around rip and replace and there was a realization that it’s not realistic.” Modernizing progressively allows banks to “move at their pace, at their budgets” while reducing implementation risk.

“We can sit on top, we can sit on the side, and so it’s a very smooth transition, and it’s a lower risk proposition for someone to want to try something new,” added Hu.

The modular approach allows FIs to start with a single product or portfolio, validate the solution’s effectiveness, and then expand their usage over time -– reducing both financial risk and operational disruption.

The pace of change in payments continues to accelerate, making system flexibility a crucial competitive factor. Financial institutions need the ability to respond quickly to market changes, regulatory updates, and customer demands.

“The way people pay is changing, and that rate of change is accelerating,” Mitchell observed. “Being able to make these tweaks or wholesale changes or launch new products very quickly is a big benefit to those that are using the system.”

The partnership’s cloud-native architecture enables this agility. “Making changes is no longer going to be ‘I submit requests to my provider, six months later, they’ll look at it,'” Hu said. “Many changes are really configuration adjustments for us. A business person can go and tweak those through your dashboard.”

Through the FIS and Episode Six partnership, FIs can adapt and react to market changes much faster, and it may also change how institutions approach product development and customer service.

The new card is just one step in PayPal’s broader commerce strategy

Even as tap-to-pay and mobile wallets become popular, the physical card isn’t going anywhere just yet. PayPal is the latest firm to reaffirm that belief, rolling out a new physical card that brings its PayPal Credit offering into brick-and-mortar stores.

The move broadens PayPal Credit’s reach, bringing it to in-store purchases, in addition to online checkouts with PayPal. It has a limited-time perk: customers can divide their payments on travel purchases over six months through promotional financing, with no minimum spend required. Shoppers can also apply for a PayPal Buy Now Pay Later loan at checkout in person. The new PayPal card is expected to roll out in the coming weeks to US customers.

I spoke with Scott Young, Senior Vice President, Global Head of Consumer Financial Services at PayPal, to learn more about the new card and how its launch signals PayPal’s broader shift from a payment processor to a commerce platform.

Doing more with less is the small bank mantra but burdened with legacy tech and consumers’ preference for digital experiences, small banks and FIs have their work cut out for them.

Especially when it comes to Gen AI.

On the one hand, the potential Gen AI offers for increasing competitiveness, CX, and efficiency demands action, on the other, are the constraints of time, money, and resources, bogging down any meaningful discussion on AI strategy.

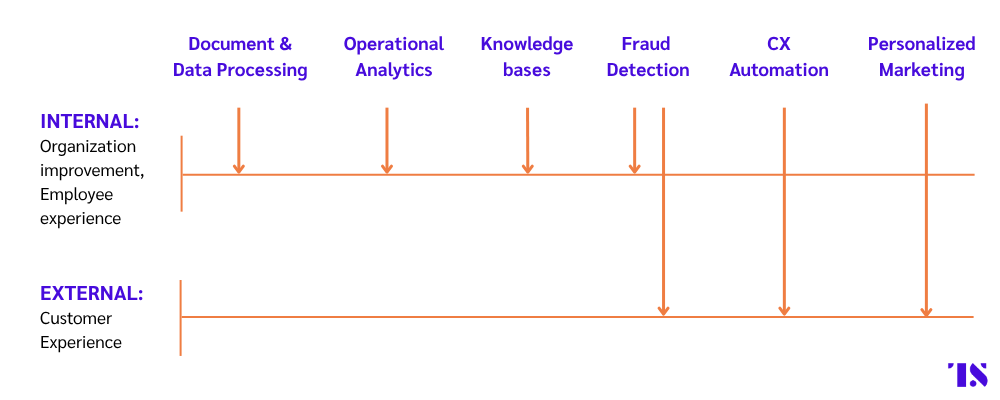

This article is the first in a series of two focused on how small banks can capture the competitive advantage of Gen AI. In this edition, we will discuss what use cases may supercharge small banks’ efficiency and customer experience and which use cases aren’t likely worth the investment for firms under $10 billion.

Use cases that work

With limited resource availability, small banks and FIs need to identify areas where they can get the most bank for their buck.

Six use cases emerge here, according to Ryan Lockard, Principal at Deloitte:

i) Fraud Detection: Bad actors are already using Gen AI to game financial systems for their gain. Criminals were able to defraud Americans out of $21 million between 2021 and 2024 using voice cloning technology the efficacy of which has been significantly improved by modern LLMs. Most big organizations are fighting this fire with fire, and using Gen AI tools to identify new types of fraud tactics as well as improve their fraud detection systems. Small banks can use these same systems to adopt real-time fraud monitoring with automated alerts to stay ahead of criminal activity.

ii) Customer Service Automation: Bank of America is about to enhance its award-winning digital assistant Erica with Gen AI. Small banks and FIs can learn from this playbook, and integrate Gen AI technology in their digital customer service agents to drive better response times and enable their staff to focus on higher-value processes.

iii) Personalized Marketing: Smaller FIs often operate with a limited marketing budget and team. Here, Gen AI tools can help better audience analytics by improving segmentation and targeting as well as help FIs create more with less through content generation.

For example, Duke University Federal Credit Union (DUFCU) recently integrated Vertice AI’s copywriting tool called COMPOSE. “The marketing team can prioritize delivering high-quality content that drives new member growth. COMPOSE is equipping us to elevate our standards of excellence, while streamlining our efforts, ensuring our acquisition campaigns are highly personalized, on-brand and efficient,” said DUFCU’s Director of Marketing Jennifer Sider.

Industry-specific tools offered by financial technology providers like Vertice are a critical differentiator here. They are trained to be compliant with financial services regulations, and can keep up with evolving regulations with relatively low-lift from FIs, and also learn from internal material to ensure messaging is in-line with the tone of the firm.

iv) Document and data processing: There is a misunderstanding in the market that just because data is available, lenders and FIs have the capabilities in place to be able to utilize it effectively. 61% of lenders report being overwhelmed by the volume of data available. Gen AI can prove to be of significant value here.

For example, the $2.5 billion, Kentucky-based Commonwealth Credit Union integrated a tool by Zest AI called LuLu Pulse, which uses Gen AI to consolidate multiple data sources like NCUA Call Reports, HMDA, and economic data, allowing the firm to gain insight into how their products and services compare to their peers.

Additionally, Gen AI-driven KYC processing can also accelerate onboarding, improving customer experience and minimizing the chance of errors.

v) Operational Analytics: Small FIs can also use Gen AI to take a closer look at the health and efficiency inside their organization. Gen AI powered operational analytics can help firms identify process bottlenecks and improve resource allocation, allowing these firms to build as much efficiency into their lean workforce as possible.

vi) Knowledge bases: Access to Gen AI-powered knowledge bases can prove to be useful for small teams, offering them quick access to information around internal policies, simplifying employees’ workflow. Banks like Citizens are already implementing such tools allowing everyone in the management chain to access information about topics like employee benefits.

Use cases that DON’T work

Given limited resources and time, small FIs need to make sure that their approach to Gen AI integrations focuses on use cases that are meaningful.

Highly complex and infrequent: Processes like complex lending decisions, where human expertise and understanding play a big role, aren’t suitable for Gen AI implementations. Low-volume, high-complexity tasks are also unlikely to yield ROI for small FIs, according to Lockard.

Poor data quality: Firms must also keep in mind that Gen AI’s output is only as good as its data. So any use cases that hinge on poorly structured legacy data aren’t a good fit for Gen AI implementation, shares Lockard. When assessing whether a use case will benefit from Gen AI implementation look for well-labelled and annotated because it allows Gen AI models to learn more quickly and produce better outcomes.

Code generation: Additionally, while people are getting excited about Gen AI’s ability to write code, only firms with in-house development teams may be able to fully leverage such features. Without in-house technical expertise to properly vet, customize, and maintain AI-generated code, organizations may face security risks, integration failures, and compliance issues that far outweigh any potential benefits.

Gen AI use case suitability checklist:

Does the use case occur frequently enough to justify investment?

Is there a clear goal and KPI that would help measure the impact of Gen AI integration?

Would the lack of human intervention in this use case severely negatively impact results?

What mechanisms are in place to take corrective action in case something goes wrong?

Who will be held accountable for mishaps?

What regulations impact Gen AI usage in this use case and is there tolerance for regulatory action against the organization?

Is the underlying data infrastructure and data ready for Gen AI integration?

Gen AI implementation holds massive potential for those small FIs that can rally their C-suite and employees to adopt the tech.

“By automating manual tasks, Gen AI drives operational efficiency, reducing both costs and error rates. It also transforms the customer experience, delivering personalized, always-on service that can rival what the largest institutions offer. But perhaps most importantly, cloud-based AI solutions empower small banks to bring new products and services to market at a speed closer to that of Universal Banks and GSIBs, closing the innovation gap and leveling the playing field.”

— Ryan Lockard, Principal at Deloitte

Identification of the right use cases is the first step in building a Gen AI strategy, stay tuned for the second part of our series to learn how to get started once the feasibility studies are over.

We will cover:

– Implementation strategies – Change management – Role of technology providers – Talent acquisition

The brakes are off, but the steering still matters

Few firms have had to earn their second chance more publicly than America’s biggest banks. Among them, Wells Fargo has been on one of the longest and most punishing roads to redemption in recent financial history.

Over the last few years, the bank has been busy rebuilding from within: restructuring leadership, simplifying its operations, modernizing technology, and tightening its risk controls. This reinvention wasn’t voluntary. Back in 2018, the Federal Reserve imposed a strict limit on Wells Fargo’s total assets, capping them at $1.95 trillion. This was all following a series of scandals, which included, most infamously, the creation of millions of fake customer accounts to meet sales targets.

Wells Fargo was barred from increasing its balance sheet because of the cap, which meant it could not:

Take on more deposits from customers (especially large commercial clients).

Make more loans to individuals or businesses beyond a certain level.

Expand trading books or grow in capital-intensive areas like investment banking.

Scale new business lines quickly, even if market demand exists.

Why it matters: In banking, growth typically comes from expanding assets: more deposits in, more loans out, more products sold, more capital at work. The cap froze Wells’ growth.

During 2018-2025, Wells Fargo likely had to:

Turn away new customers or shed low-yielding assets to make room

Prioritize efficiency and capital-light business areas (like wealth management or advisory)

Focus on fixing internal controls instead of aggressively competing in the market

In June 2025, that cap was finally lifted. After more than seven years, the bank is no longer under the growth restrictions that defined its post-scandal trajectory. This is more than regulatory housekeeping; it marks the end of Wells’ painful chapter and opens up the beginning of a new era of competitiveness.

But this development also raises a critical question: What did it cost Wells to get here? And what exactly does it plan to do with its regained freedom?