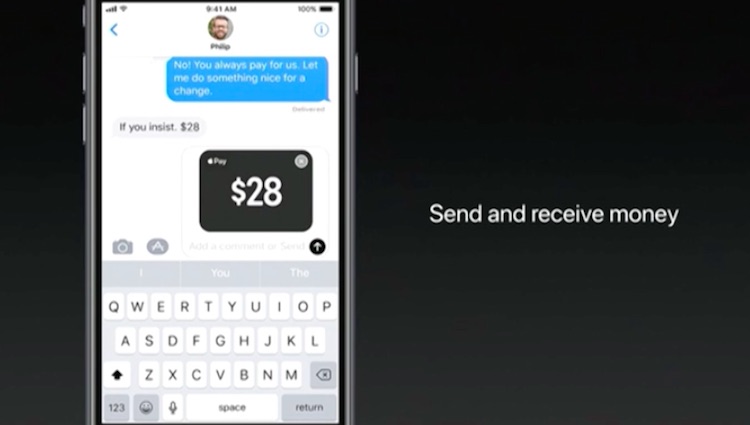

Posted on April 28, 2017April 29, 2017Venmo rising: Why PayPal wants you to pay for purchases using the app

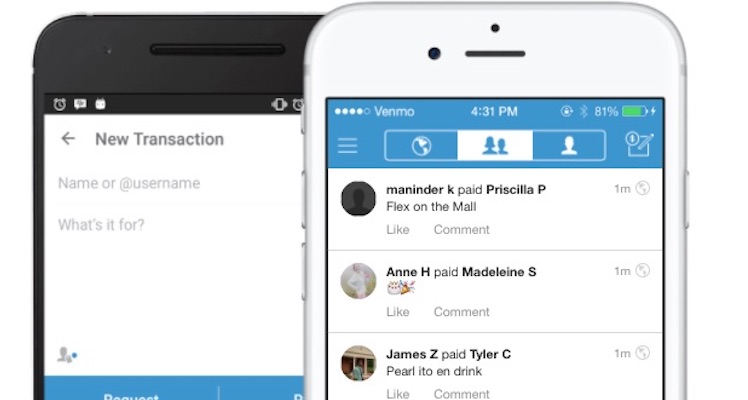

Posted on November 2, 2016November 2, 2016The 2016 Tradestreaming Awards winners: Best payments apps and technology

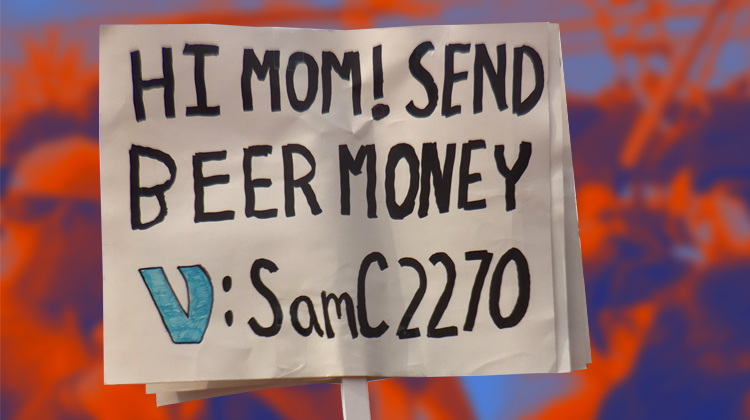

Posted on September 16, 2016March 16, 2017‘Mom, send money for fintech’: Other Venmo signs you might see this weekend on College Gameday