Search for:

Search

Latest News

Sectors

Blockchain/ Crypto

Banking

Data

Embedded Finance

Lending

Marketing

Payments

Green Finance

Conferences

Tearsheet Pro

Awards

Podcasts

Subscribe

Login

Search for:

Search

Search

Subscribe

Login

Tag:

samsung

Posted on

November 10, 2016

March 16, 2017

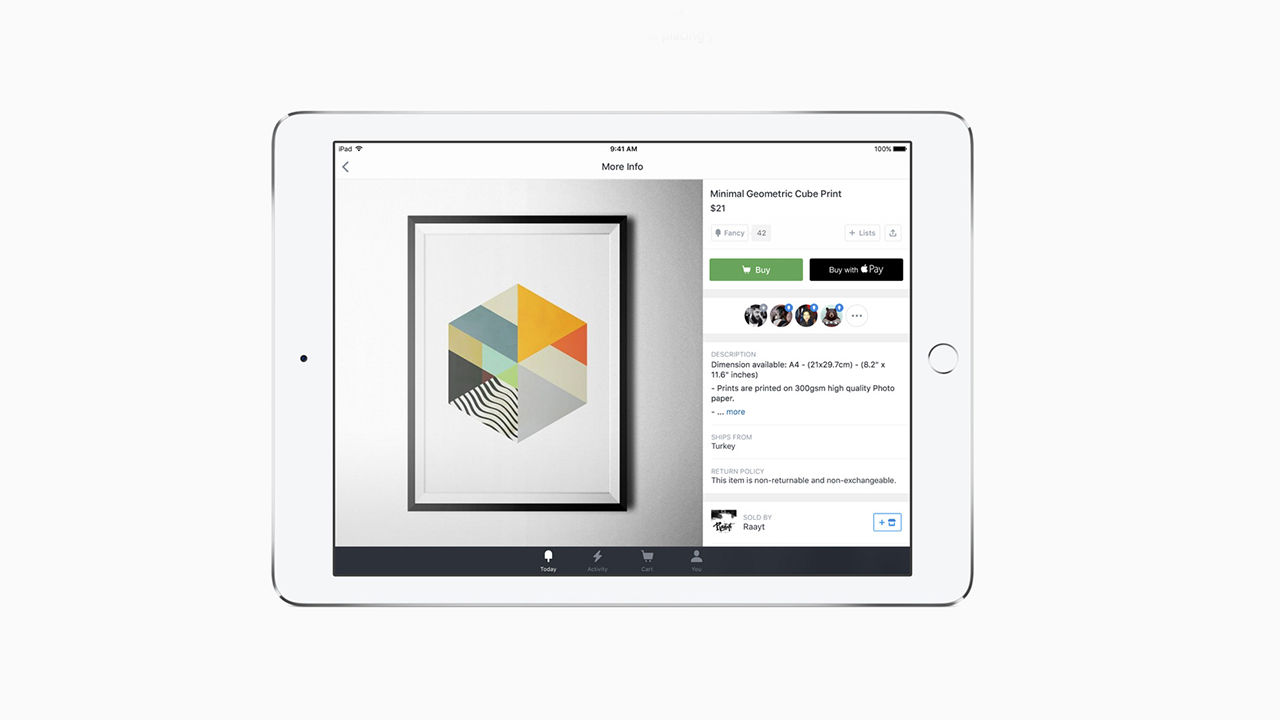

Apple Pay jumps into ecommerce

Posted on

August 29, 2016

August 29, 2016

4 charts about mobile payment growth, or the lack thereof

Posted on

July 29, 2016

July 29, 2016

5 innovative IoT payment products

Posted on

July 8, 2016

July 8, 2016

How Samsung Pay plans to compete in mobile payments