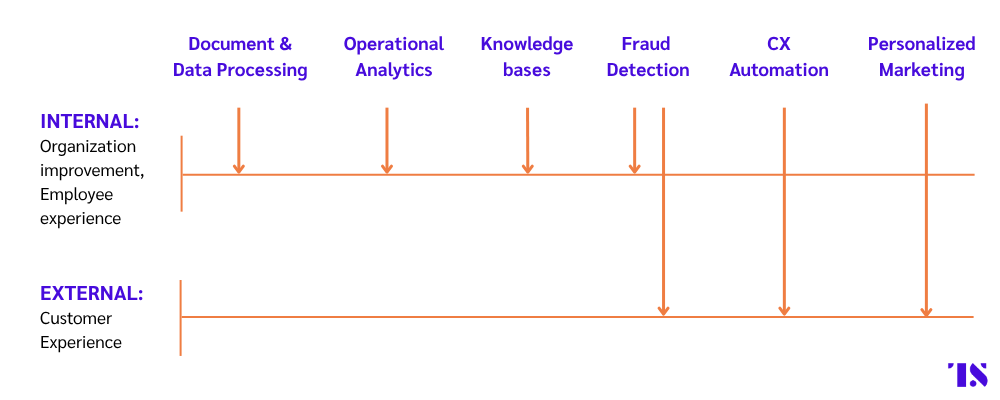

In our last article, we covered why Gen AI can help small banks remain competitive and improve six specific use cases: fraud detection, customer service automation, personalized marketing, document and data processing, knowledge bases, and operational analytics.

In this article, we will explore what implementation strategies work the best for these use cases, how to align the culture piece with the technological adoption to render plans into reality and build for competitiveness and efficiency.

The implementation playbook

Complete overhauls are difficult to undertake and don’t work well for Gen AI implementation. Gen AI is new, and the regulations, technological infrastructure, and providers around it are still developing, making a rip-and-replace approach risky.

Therefore, institutions with less than $10 billion in assets would be better served if they think bottom-up. That means identifying point solutions and specific use cases that are likely to have a sizable impact. Learnings from these roll-outs can then be used and workshopped to build a firm-wide strategy.

Ryan Lockard, Principal at Deloitte recommends the following six-step plan:

1) Identify the right use cases: Undertake an organization-wide review of which processes are likely to deliver the highest ROI post-Gen AI implementation.2) Find the right partner: Choose consulting partners, hyper scalers, and/or fintechs that have banking and compliance expertise.

3) Go API-first: Undertake an API-first integration strategy because it aids with shorter deployment times and significantly reduces disruption to legacy infrastructure.

4) Dip your toes first: Start out with a pilot project and ensure that you’re measuring and tracking ROI, so your organization can learn as much from these tests as possible.

5) Stay on top of regulations: The regulatory climate around Gen AI is likely to change considerably as the technology evolves. Small FIs can benefit from working with partners and technology providers that have responsiveness to regulations built into their systems.

Apart from what Lockard recommends, it is important for FIs big and small to recognize that Gen AI is no longer just a technological tool. It’s changing how people think of and structure their world. While the biggest players in the industry are busy touting how great the tool will be for their bottom lines, many fear job loss. In such a climate, effective, informative, and considerate communication with employees is key to ensuring that Gen AI is actually adopted and intelligently leveraged in the office.

6) Communicate learnings: Executive adoption and ownership of a Gen AI strategy is key to getting buy-in from more junior managers and the rest of employees.

Effective communication across the organization can help with adoption as well as provide opportunities for teams to identify which of their own processes could use a boost from Gen AI integrations.

How to tackle change management

Gen AI is not just changing how employees work, but is likely to reconfigure how work is done altogether. So, it’s important that employees see executives champion and lead the way forward with Gen AI usage, according to Lockard. This should involve sharing their personal observations and experiences of using the tech as well as clear communication around the importance of the vision that led to integrating Gen AI.

Firms also should recognize that Gen AI implementation may have to come with an educational component, helping employees to train and understand how the technology works. Enabling employees to overcome this learning barrier can bolster trust in the organization while also upskilling existing staff, rather than looking for new talent with AI expertise, where competition is already fierce, according to Lockard.

How to re-work hiring requirements

As Gen AI solutions become a part of the technology stack, small banks and FIs will have to rework their job specifications to include digital and partner management skills, along with vendor management, data literacy and cloud integrations for more technical roles, says Lockard.

However, unlike big banks that have started to build large AI teams in-house, small banks would be better served with maintaining a select group of internal stakeholders that can “effectively orchestrate and govern AI solutions delivered by trusted partners. Once hired, commitment to continuous learning is essential, ensuring existing staff are regularly upskilled on the latest AI tools and workflows to stay agile and competitive in a rapidly changing landscape,” he shared.

Micro case study: How Bangor Savings Bank built an employee-centric AI-strategy

Through its partnership with Northeastern University’s Roux Institute, Bangor Savings Bank announced a two-year “Accelerating Insights” program which will help build data fluency and skills in ethical AI usage among its 1100 employees. Bangor staff will get access to bespoke learning modules built by The Roux Institute, a research center affiliated with the university.

The program’s curriculum was developed through an analysis conducted by The Roux Institute, which examined organizational documents like employee role specifications and performance assessment standards, according to Liz Kohler, Managing Director of Strategy, Operations and Growth at The Roux Institute. Through the educational program, Bangor’s employees are building data fluency skills along with learning to use AI ethically.

The bank hopes that in the future, through the upskilling achieved by the program, it’ll be able to undertake much more ambitious Gen AI programs, having improved the baseline skills and performance of its staff.