Empowering people and connecting communities through remittances

- The remittance industry has evolved, reaching $800 billion in 2022, benefiting immigrants and their families with near real-time, transparent transactions.

- Digital remittances, supported by Visa Direct, offer cost-efficiency and financial inclusion, but infrastructure challenges in some regions persist, highlighting the need for wider participation in building global digital networks.

As populations shift, the remittance industry has evolved, too. Remittances have moved away from being high-friction, expensive, and low transparency to being near real-time, more cost-efficient, and more transparent. To enable this evolution, the payments industry continues to make significant strides in the types of innovative solutions, the various use cases, and the speed and costs of remittance services.

Immigration, remittances, and financial inclusion

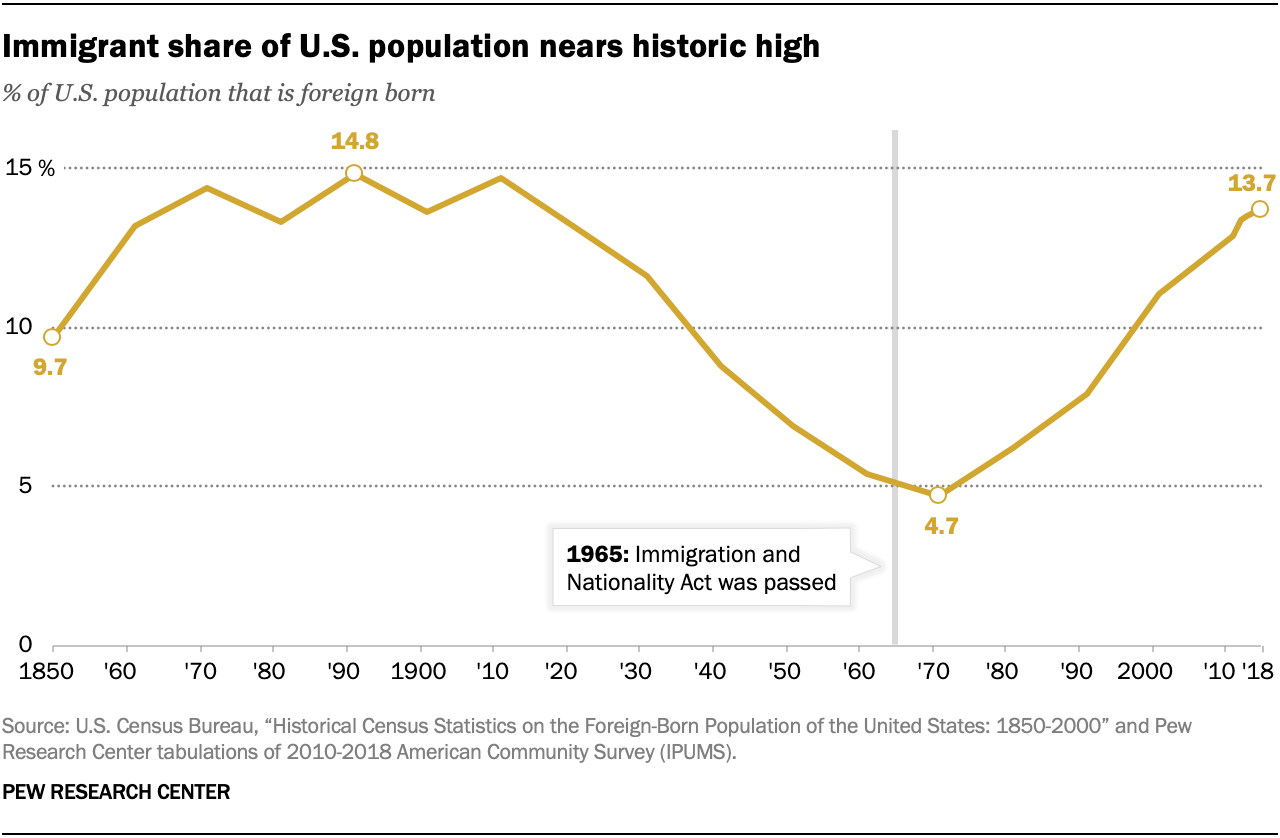

Immigration continues to change the composition of communities globally. In the United States and Canada, the foreign-born population has emerged as a significant community. The U.S. had 44.8 million immigrants as of 2020, accounting for almost 14% of the U.S. population in 2022. A more pronounced shift is happening in Canada. As of 2021, 23% of the country’s population was a landed immigrant or permanent resident. In 2030, Canada expects a quarter of its people to be foreign-born.

Moving countries requires immigrants to find ways to send and receive money. For many, remittances represent a lifeline and a means to support their families back home. An estimated 800 million people receive money from loved ones to pay for things like food, utilities, and education, according to the United Nations Department of Economic and Social Affairs data. In 2021, the World Bank estimated that remittance flows reached a new record of $733 billion. In 2022, total remittance flows were expected to reach nearly $800 billion.

When these payments are digital, they provide an additional boost to economic empowerment and financial inclusion. With advances in digital payments, families benefit from the lower cost of sending or receiving money abroad. They are able to have money available in near real-time so that they can spend it immediately on what they need.

The average cost for a $200 remittance is still over 6%, according to the World Bank. Digital payments can bring the costs down for international money transfers. They can also increase transparency for senders, so that they know the total cost of their remittances before they send.

Digital international payment flows can also lead to greater financial inclusion. With the right guardrails in place, remittance firms and lenders can work together to extend credit based on customer behavior, increasing access to financial services that immigrants lack when they first move.

“Remittances provide a way for those who are underserved or unbanked to access and use funds in real-time, creating pathways to economic empowerment,” said Jim Filice, VP, head of North America money movement and global enablement at Visa.

Looking toward a better remittance future

60% to 70% of surveyed remittance users across North America have used an app-based digital payment method to send/receive money internationally, whereas only 10% to 15% of surveyed U.S. remittance users rely on cash, checks, and money orders, according to data from Visa.

The reliance on traditional remittance methods extends beyond North America. Sending money through digital apps is the most popular method for 69% and 65% of surveyed consumers in Saudi Arabia and the United Arab Emirates, respectively, compared to digital from a physical location, cash, or check.

“With the proliferation of connected devices globally, innovation within fintechs and banks, the transformation of global remitters and capabilities of solutions developed by global payment networks – like Visa – are helping to bring seamless, secure, and rapid digital remittances within reach,” Filice said.

The plethora of opportunities for payment providers

Fintechs and new payment providers have spotted an opportunity to serve these payment flows, offering new choices for immigrants and migrant workers to send money home to their families. Expanded choices are important as research highlights how digitally enabled migrant workers can more easily compare providers and costs to choose the best options for their families.

Visa Direct is powering many of these new solutions. Visa Direct, Visa’s real-time money movement network, helps facilitate the fast delivery of funds directly to cards, bank accounts, and wallets around the world. The solution supports use cases like person-to-person (P2P) payments, account-to-account transfers, business to government payouts to individuals and small businesses, merchant settlements, and refunds.

“Money movement platforms like Visa Direct are helping to bring fast, easy, and secure remittance payments within reach, but it’s not just about streamlining payments,” Filice said. “We’re helping real individuals solve real world-problems and opening up new opportunities for financial inclusion.”

Visa Direct reaches nearly 7 billion endpoints, including more than 3 billion card accounts, 2 billion bank accounts, and 1.5 billion digital wallets. As of FY22, transactions on Visa Direct surpassed 5.9 billion.

Room for improvement

With the advances in payments technology, more people have access to digital solutions. One-third of respondents (33%) reported sending money from their home country to another country digitally, according to Visa’s Money Travels: 2023’s Digital Remittance Adoption report. That’s a 10-percentage point gain since December 2021 and an indication that digital infrastructure is crucial for successfully adopting digital remittances. But many payment corridors still lack basic infrastructure like electricity and internet connectivity, which is a barrier for millions in digitizing their cross-border payments.

With transaction volumes up, payments providers and fintechs are continuing to provide opportunities for the underbanked and unbanked, both domestically and cross-border. While remittances can improve the living conditions of those back home, they also fuel growth rates of receiving economies. In October 2022, Visa announced a collaboration with Thunes enabling individuals and small businesses to move money internationally to 78 digital wallet providers, reaching 1.5 billion digital wallets across 44 countries and territories.

“At Visa, we’re constantly striving for ways to enable everyone, everywhere to participate in the global economy,” Filice said.

Empowering the remittance landscape to be faster, more secure, more transparent, and less costly is all central to the mission of financial empowerment. However, lots of opportunities remain for policymakers, remitters, and global financial institutions to get involved. There is an urgent need to make remittances faster, cheaper, and more accessible – as they are a lifeline to billions around the globe. The payments industry recognizes the need to build up a digital remittance network that works for the people that need it the most.