How banks and consumers are responding to the distant potential of Fed rate cuts

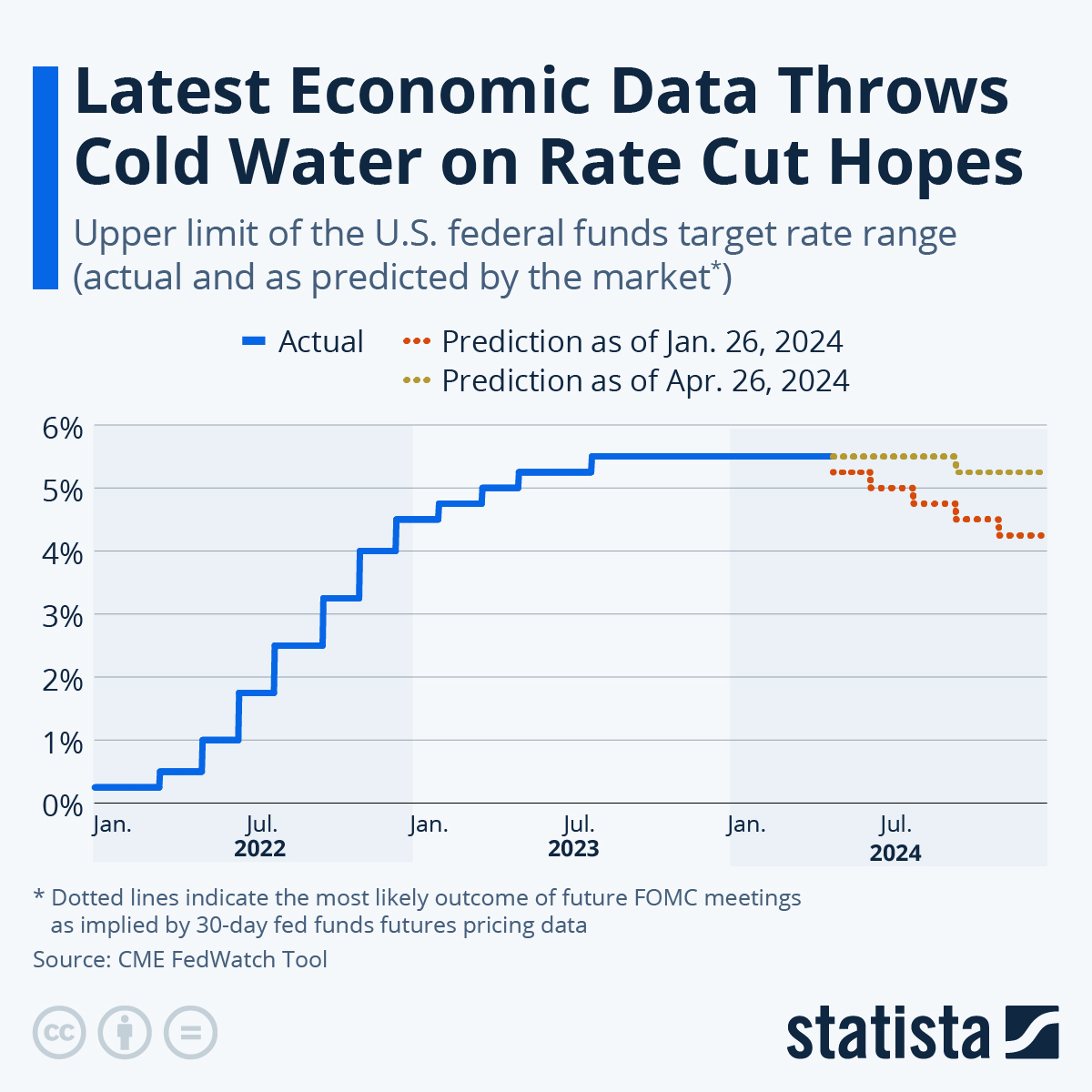

- Earlier hopes of three rate cuts in the year are dwindling to uncertainty over whether any cuts will materialize at all.

- The impact of sustained higher rates has already permeated banks’ NII as borrowing by businesses and consumers declined, coupled with higher funding costs for banks. Conversely, consumers are grappling not only with expensive borrowing costs but also with a significant portion experiencing loan rejections.

The optimism around the ease in the Federal Reserve’s combat against inflation has dissipated just one quarter into the current year.

Following the release of the Fed’s most recent projection materials in mid-March, which still foresaw three 25-point rate cuts by year-end, subsequent economic data has dampened any expectations of immediate rate reductions.

During a recent policy forum, Fed Chair Jerome Powell cautioned that interest rates might linger at elevated levels for a longer duration than initially anticipated. “The recent data have clearly not given us greater confidence, and instead indicate that it’s likely to take longer than expected to achieve that confidence,” he remarked. Powell affirmed the Fed’s readiness to uphold the current level of restraint for as long as necessary.

After a phase of enthusiasm surrounding rate cuts, markets are now responding to these developments, with earlier hopes of three rate cuts in the year dwindling to uncertainty over whether any cuts will materialize at all.

As each month passes, the continued stretch of high-interest rates is intensifying pressure on both banks and consumers alike.