Businesses are flooded with new choices of financial providers that could challenge traditional banks’ customer loyalty.

To maintain their position, banks should reevaluate their strategies and look for opportunities to integrate value-added services into their core offerings. Banks can collaborate with vendors and partners to broaden their product range and stay competitive.

Banks can take the first step by leveraging the trust they’ve built with customers to gain a competitive edge.

In the world of money, trust is the golden rule

Banks hold a strong position in the trust game with SMB customers thanks to their legacy, regulatory reliability, and long-standing reputations.

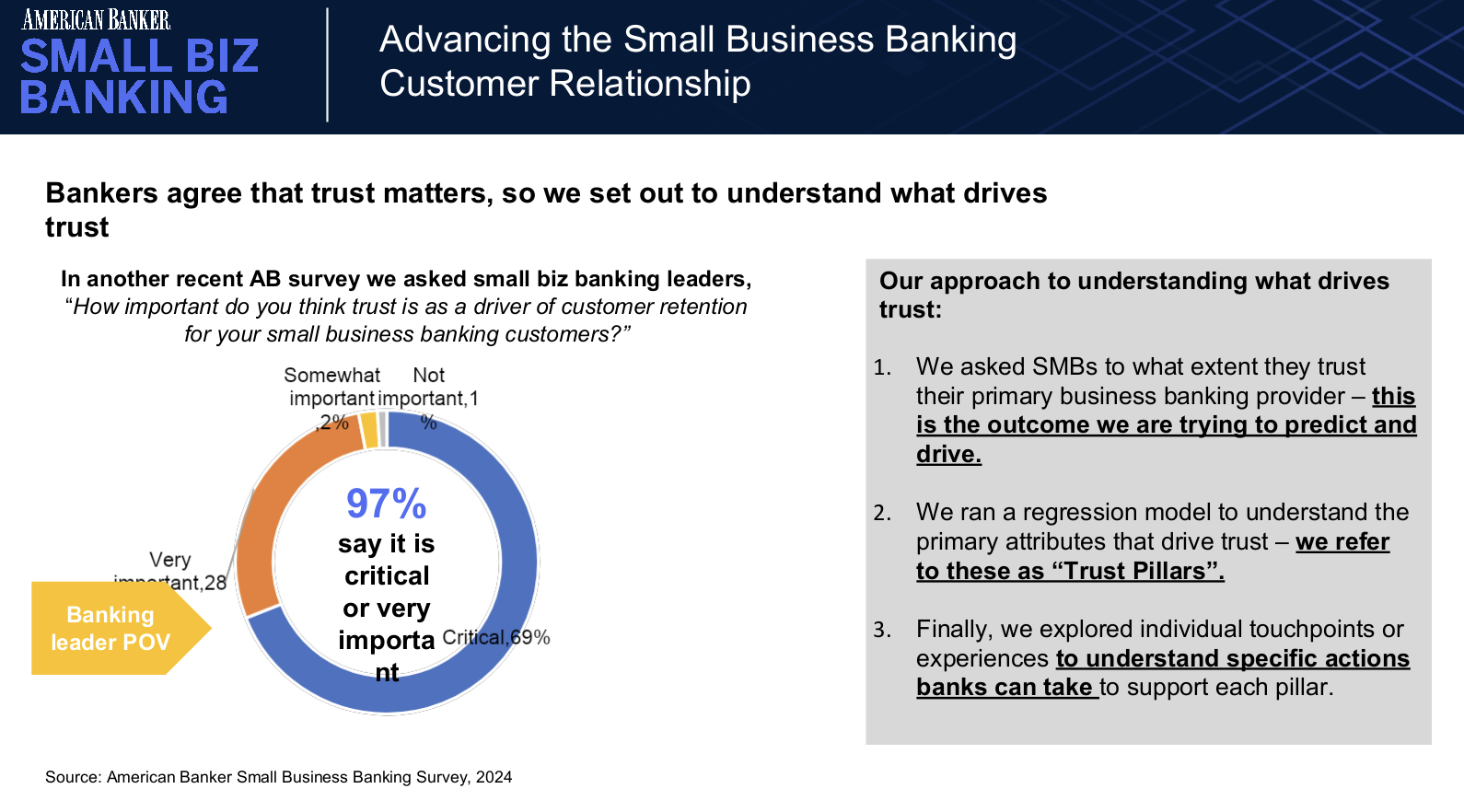

This sentiment is echoed by 97% of bankers who regard trust as a critical or very important factor for customer retention in their industry, according to research by Gusto Embedded and American Banker.

But relying on that legacy and reliability as the sole foundation for trust is insufficient to hold ground against emerging challengers.

“In addition to trust, banks need to offer additional value-added services like payroll to stay ahead of challenger banks,” said Yi Liu, General Manager of Gusto Embedded. “These businesses already trust their banks, so offering complementary services that allow them to manage all their financial needs in one place can deepen those relationships.”

SMBs expect an all-in-one solution to simplify their operations and reduce costs, so they can focus on growing their business.

According to a U.S. Bank survey, 56% of SMBs prefer a consolidated financial management platform with a comprehensive suite of banking, payments, and software solutions, and they expect their banks to provide them.

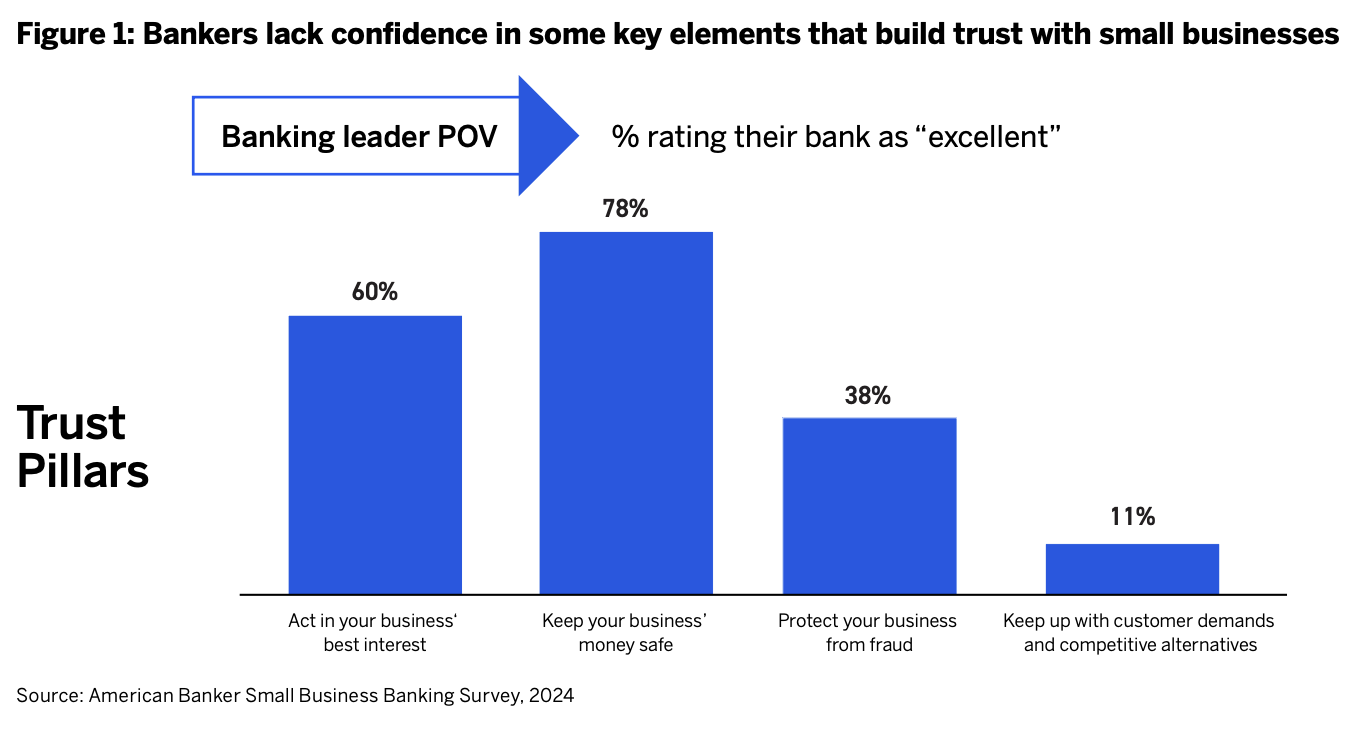

Meanwhile, banks are struggling to meet rising customer expectations and growing competition from non-bank financial institutions, with only 11% of bankers rating their banks as excellent in this regard.

This gap has prompted SMBs to explore alternatives to traditional banking. According to Gusto Embedded’s research, 70% of SMBs depend on multiple providers to fulfill their financial service needs, despite maintaining a primary bank for core functions.

Enhancing technology and unifying data can help banks break this cycle.

Banks’ rebound strategy

There is ample room for financial institutions to ramp up investment in technology, particularly in providing advanced tools for SMB owners.

Here’s how:

i) Put embedded finance at the forefront

With embedded finance solutions, banks can open doors to better serve small businesses by incorporating services like payroll processing, lending, and payment systems.

Small businesses almost universally use business checking (91%) and credit/debit cards (88%), typically through their main bank, according to Gusto Embedded’s research. Payroll services come next, with 66% of businesses using them. However, 37% of SMBs utilize external providers for payroll, while only 29% rely on their primary bank.

Banks have long held preferred provider status with SMBs. By offering embedded value-added services banks can weather industry change, gain a competitive edge, and improve customer retention, cementing their role in the evolving financial ecosystem.

“By embedding services like payroll alongside bank balance information, banks can predict a cashflow shortage and offer a loan to cover an upcoming payroll,” noted Liu. “This is a win for business owners as well, in addition to the overall time savings of having everything in one place, in one account.”

ii) Integrate superior services with minimal effort

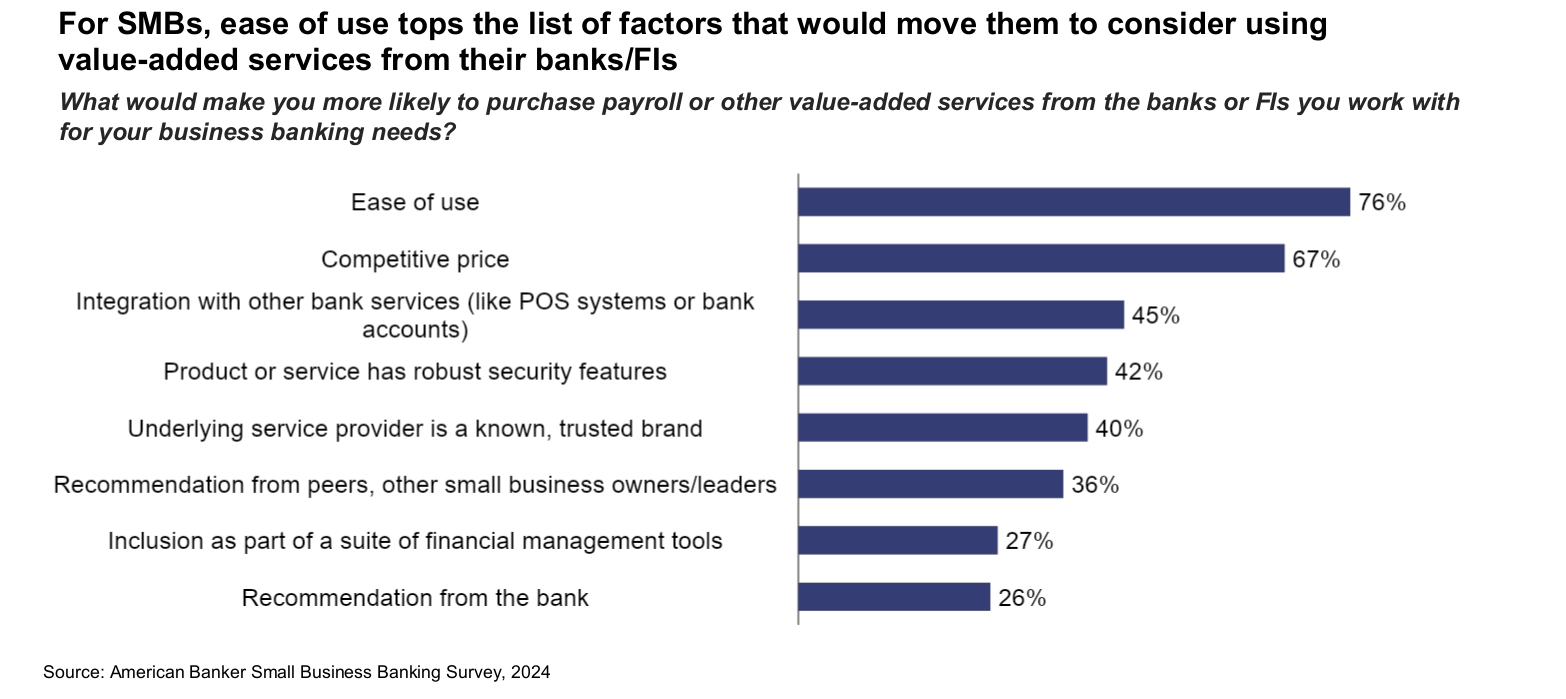

76% of SMBs emphasize ease of use as a key factor in getting products and value-added services from their banks, according to Gusto Embedded’s research.

This is a major consideration for SMBs because these businesses have limited resources and smaller teams. They need tools that are simple to integrate and compatible with their existing systems so they can avoid the complexities of managing multiple systems.

“Our customers are telling us that they’re short on time and long on problems. We do not want them to have to log into 22 different applications to run their business,” said Mark Valentino, Head of Business Banking at Citizens, during Tearsheet’s The Big Bank Theory Conference in 2024.

Additionally, SMBs typically operate in fast-paced environments, so user-friendly solutions can help them focus on their core business activities without being bogged down by complex technology or the need for extensive technical expertise.

Capturing young SMB owners’ attention with embedded VAS

Investing in tech upgrades can also help banks attract the growing group of tech-savvy young entrepreneurs, who are very receptive to convenient, digital, and embedded solutions.

Research indicates that the majority of Gen Z are eager to start their businesses ‘to be their own boss’, rejecting the traditional 9-to-5 grind. This entrepreneurial mindset is reflected in the fact that 80% of Gen Z business owners launched businesses online or incorporated mobile components, while 46% opted to start with a physical storefront.

As a new wave of young entrepreneurs enters the market, financial institutions have a chance to connect with this emerging SMB customer base by supporting their business goals through embedded VAS.

“In our experience selling payroll to small businesses, driving ease of use is critical for reaching new customers,” said Liu.

The impact of a sharp differentiation strategy

In addition to the key strategies for engaging with the SMB sector, banks can take a more proactive approach by zeroing in on solving specific SMB pain points.

Handling payroll, for instance, can be fraught with complex components. Some SMBs employ full-time workers while others rely on contractors. In fact, most small businesses have between one and five paid employees, with smaller firms typically relying more on contractors, according to Gusto Embedded’s research.

Given the various types of employees within SMBs, business owners face significant hurdles in managing payroll. Paying contractors requires different workflows and systems than paying full-time employees, adding extra complexity to payroll processes.

To create a holistic solution that tackles all aspects of a specific challenge, such as payroll, FIs can collaborate with embedded payroll providers like Gusto Embedded.

In 2023, Chase Payment Solutions tapped Gusto to offer payroll services to its business customers. By partnering with Gusto Embedded, Chase Payment Solutions customers can manage payments, banking, and payroll with a single Chase.com login. This integration streamlines payroll, tax calculations, filings, and employee paystub creation.

“When we talk to banks about embedding services like payroll, the conversation typically focuses on how banks are uniquely positioned to solve SMB pain points, such as cash flow management and real-time payroll,” said Liu. “Likewise, setting up a business bank account is often one of the first steps for new business owners, followed by accepting payments and then payroll.”

“So, it makes sense that all of these services are available in one place.”

Learn how to create customized products that meet the payroll needs of diverse SMBs to solidify your connections. Download the Gusto whitepaper here.