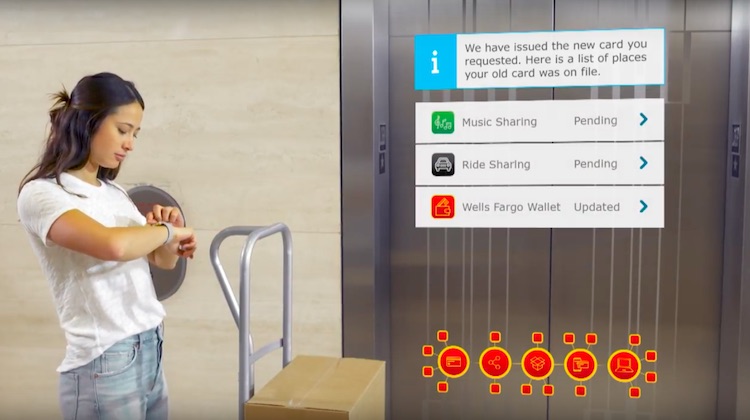

Posted on July 24, 2017July 25, 2017How Wells Fargo is letting customers take back control of their financial data

Posted on May 17, 2017May 18, 2017‘The biggest challenge is the distraction over disruption’: FIS chief product officer Rob Lee