Posted on August 30, 2017August 29, 2017Banks are falling behind when it comes to understanding — and using — data

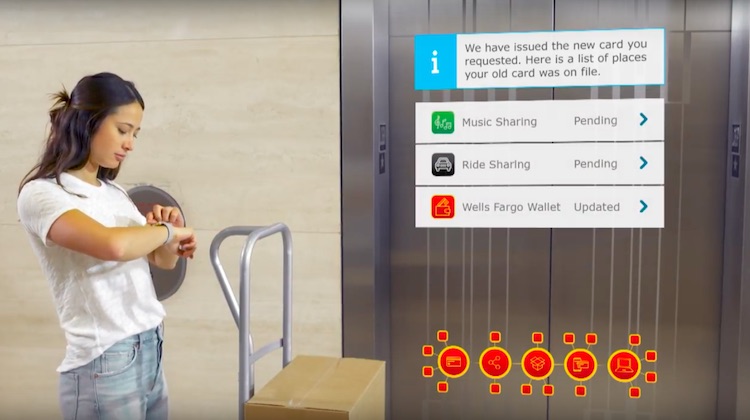

Posted on July 24, 2017July 25, 2017How Wells Fargo is letting customers take back control of their financial data

Posted on May 12, 2017May 16, 2017The biggest challenge to secure data access is time: Xero president

Posted on March 3, 2017March 16, 201710 years on: Once a first mover, Mint must work to stay relevant

Posted on June 16, 2016July 6, 2016Behind closed ledgers: an inside perspective on the Wells Fargo / Xero integration