The Customer Effect

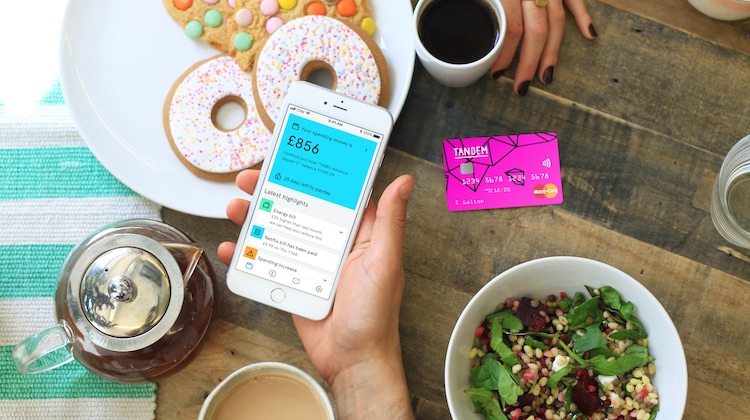

Why UK bank Tandem acquired personal finance startup Pariti

- U.K. challenger bank Tandem acquired personal finance startup Pariti in an effort to build out its features

- Tandem's move is a way to keep control over its mobile app's personal finance capabilities and create room to differentiate among a sea budgeting apps