The Customer Effect

Capital One is using Foursquare to push offers to customers

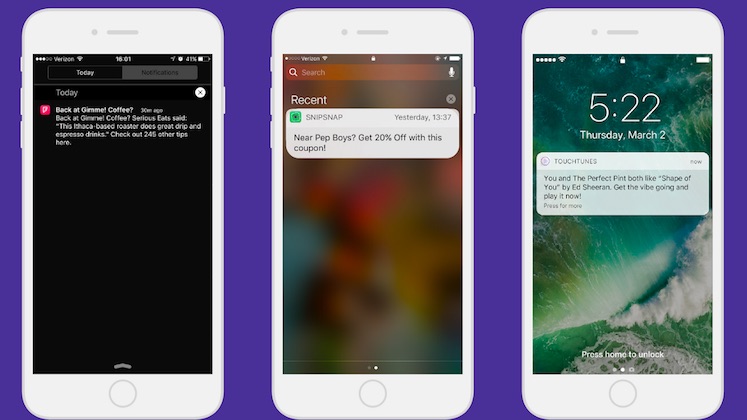

- Location-based data and analytics platform Foursquare is helping banks deliver location-based offers to customers at partner retailers

- Location-based marketing can be a valuable tool to raise the profile of a brand, but there are issues with permissions and seeming too intrusive to the customer