Fewer branches and loan products are amplifying customer turnover for CUs

- Despite the rise in digital banking adoption, consumers are reluctant to entirely abandon traditional brick-and-mortar branches and face-to-face interactions, particularly those who primarily use CUs for their financial needs.

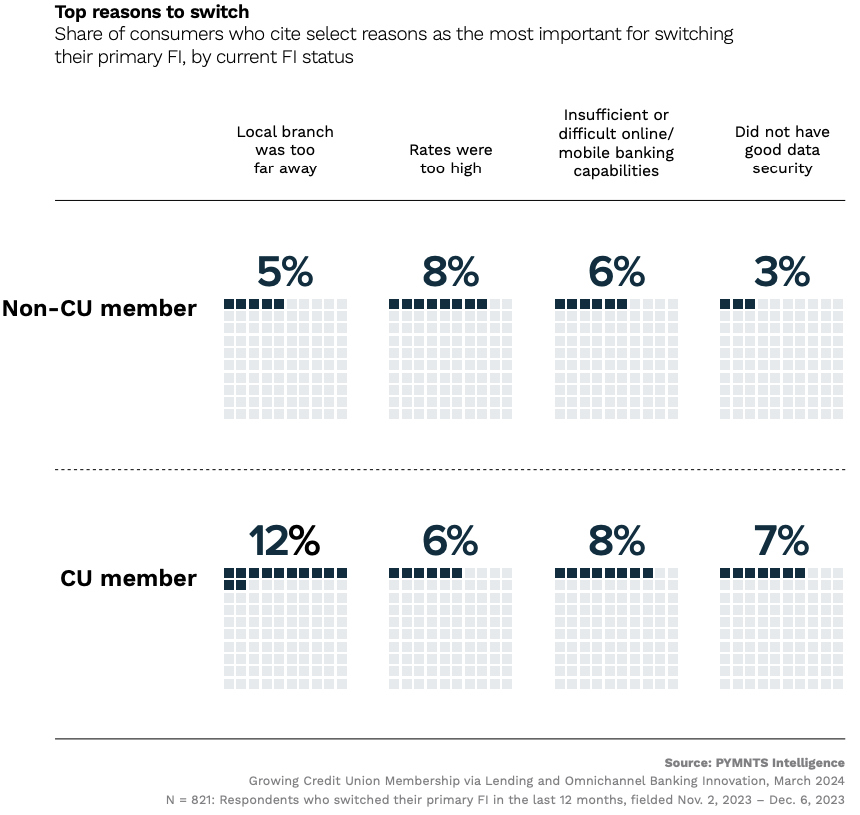

- CUs may risk losing customers, though, to banks that often have more branches and ATM networks, better online and mobile app technologies, and a wider range of products.

A growing majority of Americans are embracing digital banking options, with 71% choosing to handle their bank accounts through mobile apps or computers. This preference was also notable among consumers of major banks like Bank of America, JPMorgan, and Wells Fargo, as indicated by their financial results in the final quarter of 2023, underscoring the shift toward digital.

Despite the upward trend in digital banking adoption, consumers are hesitant to completely forgo traditional brick-and-mortar branches and personal interaction when addressing complex financial needs, especially those who rely on credit unions [CUs] as their primary financial service providers.

In fact, according to a recent report by PYMNTS, the lack of local branches and subpar mobile apps are the top two reasons 1 in 5 CU consumers switched financial service providers in the last year.