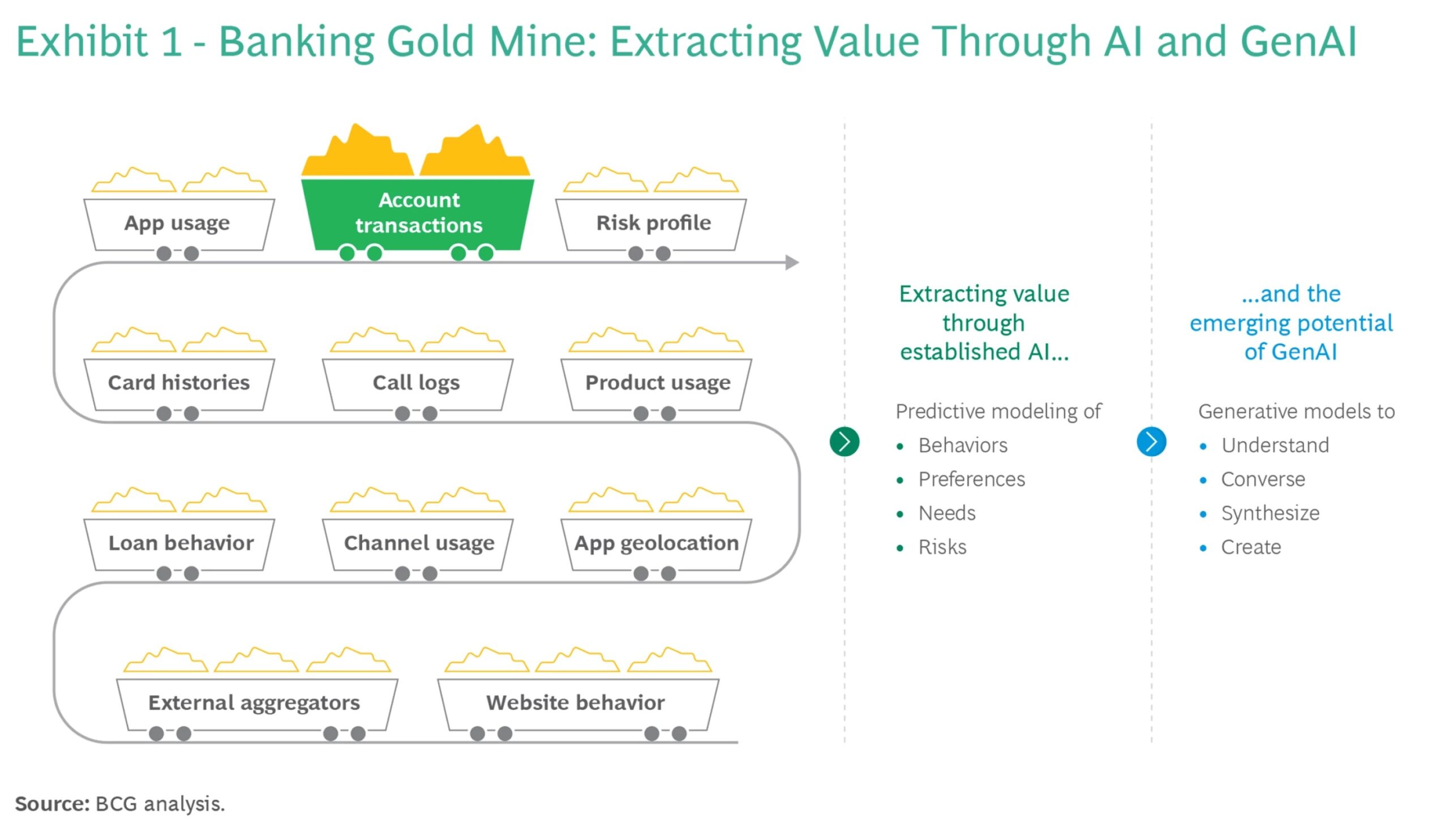

Letter from the editor: Some thoughts on AI and financial services

- Beyond the hype of AI, will banks really be able to harness any of the new tools to improve customer experiences and products?

- From Mastercard to Key Bank, it's clear that AI's first stop isn't anywhere near its last.

“I always get extremely excited about a new technology, but I’ll call it a measured, perhaps even a jaded, enthusiasm, because over the years, there’s been so many technologies that are out there. I remember, it’s probably a dozen years ago, people had to end every sentence with and on the blockchain. And you’d have to ask: why is it better than what you have?” – Mastercard CTO Ed McLaughlin on the Tearsheet Podcast

My conversation with Mastercard President and CTO Ed McLaughlin this week helped to put some things in perspective around new technology. You can listen to the whole episode and get the transcript (available only to TS Pro subscribers).

Every few years, there are tech trends that get everyone excited. Part of that is vendor pressure that focuses on point solutions. Part of that is FOMO built and nurtured by financial services consultants supported by data and research. Innovation teams have to demonstrate that they’re getting their hands dirty with the next, new thing. The media is involved, too.

The reason that the steak typically doesn’t match the sizzle when it comes to the tech fads our industry experiences is that the whole adoption curve is typically upside down. Frequently, in the beginning, there are technologies looking for a use case, rather than the other way around.

Think blockchain a couple years ago. Chatbots a few years before that.

Where AI fits in

AI is that technology right now.

Not everyone sees a massive opportunity. Gartner placed generative AI on the Peak of Inflated Expectations on the 2023 Hype Cycle for emerging technologies.

Are things really different this time around with AI?

To be able to answer that, we have to look at:

- Better than alternatives?: whether our needs are best served by this new tech (or said differently, is it better enough than existing ways I’m solving my problem).

- Value of tech: Is the tech really ready for prime time?

Needs assessment comes before tech evaluation

Here’s Mastercard’s McLaughlin again on the needs assessment that precedes tech adoption: