Fewer branches and loan products are amplifying customer turnover for CUs

- Despite the rise in digital banking adoption, consumers are reluctant to entirely abandon traditional brick-and-mortar branches and face-to-face interactions, particularly those who primarily use CUs for their financial needs.

- CUs may risk losing customers, though, to banks that often have more branches and ATM networks, better online and mobile app technologies, and a wider range of products.

A growing majority of Americans are embracing digital banking options, with 71% choosing to handle their bank accounts through mobile apps or computers. This preference was also notable among consumers of major banks like Bank of America, JPMorgan, and Wells Fargo, as indicated by their financial results in the final quarter of 2023, underscoring the shift toward digital.

Despite the upward trend in digital banking adoption, consumers are hesitant to completely forgo traditional brick-and-mortar branches and personal interaction when addressing complex financial needs, especially those who rely on credit unions [CUs] as their primary financial service providers.

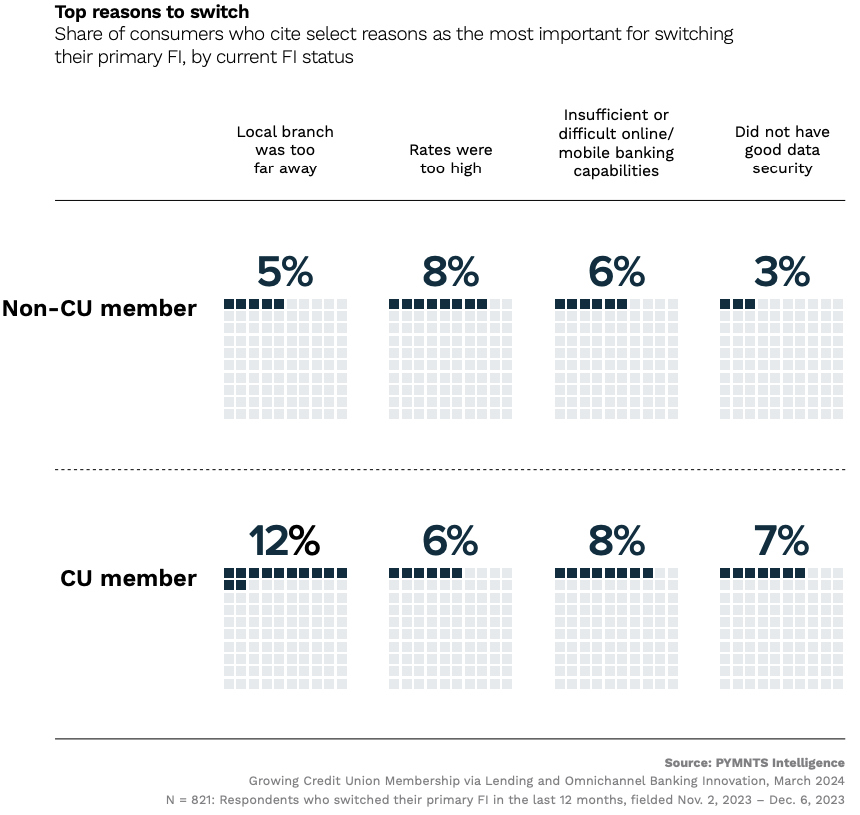

In fact, according to a recent report by PYMNTS, the lack of local branches and subpar mobile apps are the top two reasons 1 in 5 CU consumers switched financial service providers in the last year.

While a subset of consumers may lean toward CUs instead of traditional banks due to lower interest rates on loans and fees, data indicates their readiness to switch providers should their financial needs remain unfulfilled or if they find superior services elsewhere.

This also serves as a reminder for CUs, which may risk losing customers to banks that often have more branches and ATM networks, better online and mobile app technologies, and a wider range of products. Consumers expect a smooth banking experience, whether online or in person, reiterating the importance of modernizing branches to meet evolving client needs.

Sticking to traditional offerings contributes to the mix of customer attrition

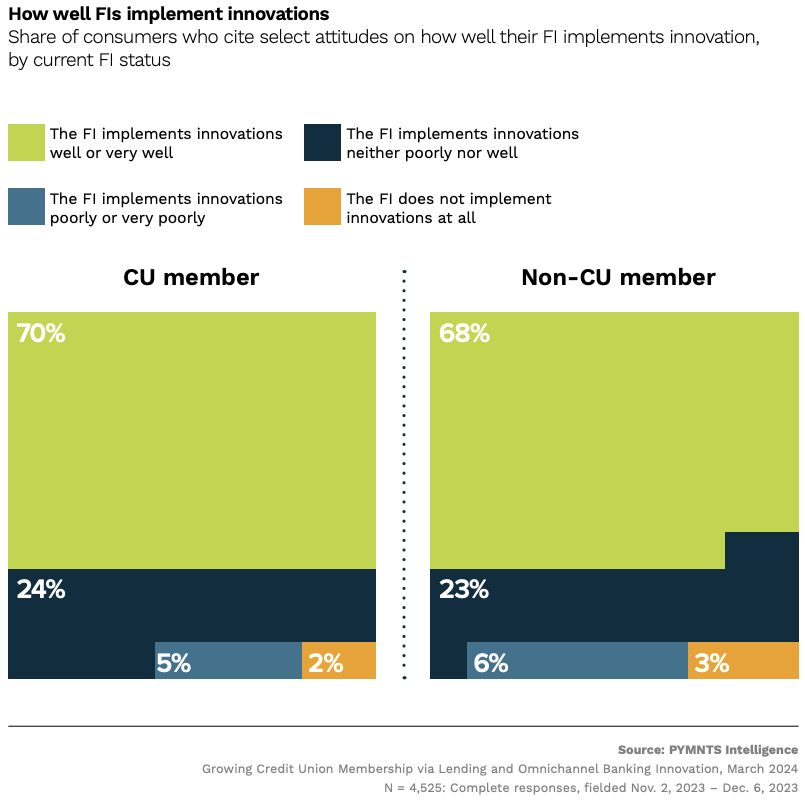

Another contributing factor to customer turnover in CUs is the pace of introducing new products and services. While 70% of members have high expectations for innovation from their credit unions, there’s a clear gap in the speed and consistency of new product launches and upgrades. Merely 7.7% of CU members indicate that their FI introduces new products and services ahead of others.

This presents an untapped opportunity for CUs to minimize member attrition and attract new customers by zeroing in on improving and delivering new and more personalized offerings to compete with traditional banks and align with consumer expectations.

According to the report, CU customers highly value personal loans and split-payment offerings when selecting a financial institution, a preference that also extends to other lending products. 25% of credit union members want their credit union to expand the product suite on personal loans, while 21% want the same in auto loans over the next three years. There’s also strong consumer demand for Buy Now, Pay Later [BNPL], with 17% of credit union members wanting their FI to focus on this area.

Although CUs have been adding new lending products to their product portfolio, there’s been little departure from traditional offerings in personal and auto loans. While nearly all [99%] of them currently provide these loans, only a scant few (1.5%) offer short-term financing options like BNPL, indicating a cautious stance toward alternative split-payment plans.

Despite mounting consumer interest, it appears that offering BNPL isn’t a top priority for many CUs. While 31% plan to introduce installment loans within the next three years, 18% anticipate doing so within the subsequent six years. This shows almost half of the CUs have no immediate plans to offer the pay later service, placing them at a disadvantage if BNPL adoption continues its upward trajectory spanning the next three to six years.

The report further accentuates CU consumers’ interest in technological upgrades, emphasizing the need to integrate cash flow management features like budgeting tools, QR codes, and voice assistants into their existing financial institutions.

By identifying and addressing discrepancies between customer expectations and the services provided, CUs have the opportunity to develop new strategies to provide financial solutions that address members’ unmet needs. Embracing this approach could result in increased customer engagement and loyalty while attracting new ones into the fold.