We have entered a period of what Google’s chief economist, Hal Varian, likes to call “combinatorial innovation”; a term for when many factors combine to drive the creation of new inventions. Today, the key factors sparking innovation are transparency of information, speed and connectivity, open source software and APIs which enable the development of layered ecosystems of applications. One such innovation that was created by the coming together of these factors is the blockchain.

The blockchain serves as an append-only data store of transactions that has two components: a replicated ledger and a distributed database. The database is stored and synchronized by all parties (referred to as nodes) to a shared ledger within the blockchain network. Bitcoin, a digital currency that uses blockchain technology, is used to track money transactions but it can also track the exchange of other assets including financial securities or data related to an individual’s identity such as IDs or proofs of address, for example.

Blockchain is far from being a passing fad and finance professionals need to become familiar with the concept because, in time, it is likely to fundamentally overhaul the way financial transactions are made. Indeed, once it begins to be adopted more widely, it will revolutionize the structure of the financial services industry as the technology eliminates the need for trusted intermediaries such as clearing houses. Financial institutions that are not exploring the opportunities that blockchain creates will lag behind in terms of knowledge and strategic options, particularly in relation to efficiency and cost saving opportunities. Further, front office systems automation, as well as the simplification and standardization of back office systems, are areas that are likely to take place as a result of blockchain technology implementation. Financial institutions, therefore, have duty to look to innovative technology solutions the adoption of which may be more imminent than is currently understood.

GreySpark is currently exploring seven capital markets’ use cases for the blockchain:

The most pertinent use cases, in GreySpark’s opinion, are in clearing and settlement, reconciliation and the use of smart contracts.

Smart contracts are event-driven computer programs that allow the automatic verification of the transactional governance (terms and conditions) between two counterparties, eliminating the need for a central arbitrator. Smart contracts can be added to blockchain-based transactions to deal with the legal aspects of a commercial agreement.

The use of blockchain technology will mean that the execution, clearing and settlement of a trade can occur quasi-instantly, lowering post-trade latency and reducing counterparty exposures. Blockchain transactions are quicker, less expensive and involve fewer intermediaries such as brokers and central securities depositary that the traditional approach.

Blockchain technology can also be used to simplify the reconciliation of trades as this approach does not require the comparison and rectification of ledgers held by different institutions. In the case of a private blockchain, where participants gain permissioned access to the database, institutions are able to meet their reconciliatory obligations without actually having to reconcile with other institutions, thanks to the replicated and synchronized nature of the blockchain ledger.

It will, however, take some time for the scale of blockchain applications to reach a critical size. As it is at an early stage of development, the excitement it is generating in the industry is a normal thing, but the first step into this new world, such as investing in blockchain start-ups for example, must be taken with great care: lucidity and a comprehension of the implications will be a key success factor in this area.

While the applications for Distributed Ledger Technologies for each use case are equally valid, some of the use cases have already proven to be stronger than others. These offerings are capable of either disrupting or replacing existing trade-lifecycle technology systems and processes in banks and financial markets infrastructure providers such as clearinghouses and exchanges.

GreySpark believes a starting point for the industry should be to focus on developing ways of employing blockchain technology to improve the process of transferring securities by enabling market participants to connect on a peer-to-peer (P2P) basis without the intermediation of brokers. This would remove friction and allow the execution, clearing and settlement to occur at a trade-entry level, quasi-instantaneously.

When trying to turn the transfer of securities into a real P2P blockchain-based system, the challenge lies in taking the whole trade lifecycle into consideration to ensure the process is seamless. For instance, from the technology perspective, this includes being able to digitize securities and map share registers on the blockchain. Another challenge is to ensure the blockchain technology is scalable enough to deal with tomorrow’s transaction volumes. To address this, companies such as SETL are developing solutions to extend bandwidths and increase block capacities.

In 2016, people will begin to focus on, not only defining proof of concepts, but on the development of operational and productive applications. A carefully investigated proof of concept will enable firms to identify vendors that are right contenders for executing their blockchain program.

Also, increasing numbers of financial institutions will reach out to consultancies like GreySpark to help them to adapt to innovative technologies, assess emergent players and understand the risks associated with the new technology. Clients will be equipped with strategic plans to help them both understand and gain competitive advantage of the evolving technology environment. To address emerging trends and face innovation challenges in the Capital Markets industry, major financial institutions need help in deciding whether they should build in-house systems, collaborate with existing key players or invest in or directly acquire them. Ignoring the new concepts and innovations is an option financial institutions can no longer afford.

William Benattar

William Benattar is a member of GreySpark’s fintech advisory team. By maintaining a comprehensive view of the fintech arena, William assists GreySpark in helping start-up firms enter the marketplace; advises private equity houses on financial technology due diligence; and advises buyside and sellside clients on the development of strategic and innovative projects . Prior to joining GreySpark, William worked for Kantox in the business and product development team, focusing on strategy developments of FX systems. While being student ambassador for Google, William has spearheaded initiatives aimed at helping SMEs develop and implement their digital strategies. William is an existing mentor at the London-based accelerator program — Startupbootcamp Fintech — advising start-ups on product development, roadmapping and fundraising avenues.

GreySpark Partners

GreySpark is a business and technology consultancy that specialises in mission-critical areas of the Financial Markets industry with offices in London, New York, Hong Kong, Sydney and Edinburgh. GreySpark has expertise in Electronic Trading, Risk and Trade Management, Operations and Data Management and provides Business and Financial Technology Consulting services to buyside and sellside businesses as well as exchanges, market data providers, Independent Software Vendors and technology makers.

GreySpark recently published a report entitled The Blockchain: Capital Markets Use Cases.

Photo credit: Marko via VisualHunt / CC BY

If you listen to NPR, you’ll sometimes hear a recording artist, someone like Lyle Lovett, referred to as “an artist’s artist”. Meaning, an artist that other people of the same craft can appreciate and love.

Our guest on this episode of the Tradestreaming Podcast is an analyst’s analyst. For the past 25 years, Ron Shevlin’s worked with the leading financial services, consumer products, retail, and manufacturing firms in the world. Ron’s the Director of Research at Cornerstone Advisors, a consulting firm to the banking and credit union industries, where he specializes in retail banking issues including sales and marketing technologies, customer and marketing analytics, social media, customer experience and consumer behavior. He was previously at Aite and Forrester covering the financial services space.

Most importantly for us, he’s the author of weekly articles he calls Snarketing published on the Financial Brand website that combine his keen eye for trends and opportunities for growth in the financial services space with his great sense of humor. It’s a must read for me and I hope it will become part of your reading list, too.

In this episode, we:

Photo credit: COMSALUD via Visual hunt / CC BY

[dropcap size=big]W[/dropcap]hile the stock market opened 2016 with a loud plop, the hottest companies continue to be technology startups. Atop this pile sits Uber. Uber has become synonymous in tech circles for how easy buying things really can be and how enjoyable the experience can be, as well. If the taxi industry can be Uber-ized, the thinking goes, so can many large industries that have similarly been slow to change.

This conversation hit finance circles when the WSJ ran a story about how slow the finance industry has traditionally been in adopting best practices that have influenced the buying cycle in other industries. According to the article’s author, Zachary Karabell, head of global strategy at Envestnet, finance is indeed now undergoing its own Uber process. Not overnight or over weeks and months, but over the next few years, major parts of finance will undergo technology-driven disruption. And this change is being driven by fintech startups, like Wealthfront, EquityZen, Loyal3, and ZestFinance.

Whatever the risks, however, the Uberization of finance is no fad or stunt. Many of today’s startups may implode, as most do, but the spread and democratization of capital—and the proliferation and analysis of data—are irresistible trends. They will offer new opportunities to millions of people, entrepreneurs and investors alike. They also will unlock a vast amount of money, energy and talent, and to that we simply should say, bring it on.

Not everyone buys this line of thinking. Cornerstone Advisors’ Ron Shevlin explains that there isn’t really a parallel to the financial industry because this whole discussion is based on a misunderstanding of what Uber has really done. Uber pursued a consolidation strategy in a highly fragmented industry. The WSJ cites marketplace lending and crowdfunding as examples of uberization but rather than consolidate, these new forms of finance add to the fragmentation of the finance industry.

Upstart, an online lender targeting millennial borrowers, is typically used as an example of the disruptive change that’s happening in finance. In order to lend to young adults, Upstart had to turn traditional lending models on their heads, as many of these FICO-like credit scores rely on historical data. As young people find their places in the gig economy, it’s not easy for them to get loans. Upstart’s forward-looking models are trying to change that. Young borrowers don’t have very much credit history, so Upstart uses other inputs to determine creditworthiness for its customers.

Mike Osborn joined the startup finance company recently as the company’s first CMO. Hailing from the marketing team at Uber, Mike joins a firm that’s generated $240M in originations in 18 months since it launched, averaging 25% month to month growth since inception (you can listen to Tradestreaming’s interview with Upstart founder and ex-Googler David Girouard below).

Osborn has a quick 3 point questionnaire when testing for Uberization:

Finance fits this model, and to Osborn, much of the change is going to happen from the bottom up — with changes in consumer usage patterns brought about by top UI/UX in new finance apps and platforms. “When you think of what drives user experiences, in Upstart’s case, it’s about having better holistic models, better rates, different options — all with the view that we’re helping our users out of a jam,” Osborn explained.

In this vein, next generation finance tools should resonate with users and generate the same reactions as other apps residing on their smart phones. Why shouldn’t users have the same visceral responses to their banking apps that they do to their transportation apps?

“When your target audience are millennials, they live and breathe online and they do it in a community-driven way. Financial service providers need to find ways to get their users financially fit and package it into a shareable experience and celebrated event — the same way getting physically fit is. When someone loses a lot of weight and gets in shape, they take a before-and-after picture and post it socially. I can imagine the same thing happening before and after a difficult credit card situation.”

Perhaps ironically, many of today’s online financial services startups rely on offline methods to acquire new customers. It’s especially acute when it comes to landing new borrowers, as two of the largest online consumer lenders, Lending Club and Prosper, each send tens of millions of offers via snail mail every month. Upstart’s Osborn embraces both online and offline acquisition marketing.

“When we think about where we’re going to find our next customers, we’re definitely looking at the offline opportunity. We’ve been positively surprised in volume and profitability with offline channels. When you get an email offer to refinance your debt, it’s pretty easy to ignore it. But when you get your credit card statement in the mail and a couple of days later, receive an offer to help pay it off, the offer has relevance and timeliness when it comes via direct mail.”

Same goes for social media marketing. Osborn claims that a Facebook response is either immediate or it disappears into the ether. That’s not to say Facebook isn’t fertile ground to message new prospects — it just needs to work quickly. Same goes for Google and search engine marketing. “The economics on Google work but we’ve been most positively surprised with direct mail,” Osborn reasoned.

It’s debatable whether the disruptive change everyone’s talking about is supply-side or demand-side driven. Osborn thinks it’s actually a confluence of factors that’s enabling the next generation of financial services, technologies, and apps racing to get a foothold with today’s customers.

Osborn believes it takes a new type of company and leadership to be able to compete today — both require an understanding of big data and large systems. “When I first met with Dave and the rest of the leadership team, founded by Googlers, I saw they understood the power of taking in all that data and making wise and powerful decisions, like extending credit, with it. There’s a reason we have such good ratings on CreditKarma and high NPS scores with our customers.”

Whether financial services are actually being Uber-ized misses what’s really going on. Led by technology advances and driven by customer demand, startups and incumbent institutions are changing the way users interact with money.

Photo credit: FamZoo via Visual Hunt / CC BY-SA

Andres Wolberg-Stok is the Global Head, Emerging Platforms and Services at Citi.

The most impactful thing happening today in banking -and in fact it’s happening not just in banking but across pretty much every consumer-facing industry- is the digitization and the user-experience revolution. Now that we all spend so much of our time on our smartphones, those apps we use all the time have reset the bar for what we expect of every interaction. We all demand that everything be as simple and intuitive as the best apps out there from digital companies. It sets a really high standard for everyone else to strive for, and in some cases it requires a reinvention of the entire underlying process. And all of that is a good thing, of course.

At Citi, we are always looking for ways to put our clients in control of their finances and to help them bank however and whenever they want. We’ve been on a journey of innovation for decades, led by that principle, working to bring your accounts ever closer to you. We pioneered the ATM in the 1970s, so you wouldn’t even need to step inside a branch. We were one of the early leaders in online banking, in the early oughts, so you could bank from home or from your office. We were the first major U.S. bank to offer a downloadable mobile banking application, back in 2007, putting the bank in your pocket. Last year, we became the first major U.S. bank to offer no-login access to your accounts (we were issued a U.S. Patent for that this year). And as you point out, this year, we became the world’s first bank with an app for the Apple Watch. You can see the progression, right? Ever closer, ever more available and closer to you. Wearables are here to stay, and your money has a rightful place on them. I just don’t know what we’ll need to do in order to get closer to you next time — what’s next, banking implants?

Citi is the world’s leading global bank. We operate in some 160 countries or jurisdictions, with consumer operations in 24 markets at this point. Globality is in our DNA, and it helps us cross-pollinate the best ideas from our colleagues around the world. It also allows transfusions of talent, and of regional perspectives, around the globe, and it helps us serve well those of our clients who are global themselves. To be succefully global, you have to be global and you also have to be local everywhere you are. In fact, together with digitization and urbanization, globalization is one of the three major strategic themes that drive our work.

The bank of the future recognizes that every man, woman and child carries a supercomputer in the shape of a smartphone. It knows people want to pick and choose their experiences, and that they probably do not want to depend for everything on a single supplier of financial services. The bank of the future is the one that understands how to become a whole-life partner for every one of its clients, how to earn a spot at the heart of their individual web or assembly of financial services, and how to be by their side every step of the way for their day-to-day needs as well as for the major moments in life. That bank of the future works with, not against, the fantastic ideas coming out of the Fintech ecosystem – it figures out how to become an integrator of Fintech value for its clients. That’s what, here at Citi, we call “Fintegration”: the integration of Fintech. Banks have the heavy compliance machinery, the track record, the know-how to keep your money safe. Fintech companies can come up with great new experiences, and they need the scale. Fintegration is a win-win all around, starting with the client.

Traditional banks are finding out new competition lurks everywhere.

Pureplay startups like marketplace lenders, Lending Club and Prosper are originating billions of dollars of loans every quarter. Though volumes are small compared to total SMB outstanding loans (which in 2013 stood at $585 billion), some banks are turning to the marketplace lenders to buy loans, opting to partner instead of compete.

This move towards alternative lending, core to banking services, isn’t just a US phenomenon. Funding Circle, another leader among the current class of startup online lenders, has global aspirations.

Funding Circle’s co-founder, Sam Hodges recently explained to Tradestreaming:

Our vision for Funding Circle is as a global lending exchange, where business from all over the world come to find finance from an army of investors, big and small. Small businesses are underserved in most of parts of the world, and we believe our marketplace model can help millions of businesses and investors to get a better deal. At the moment, we are focusing all of our energy on building a successful business here in the UK, USA and Europe.

There are high hopes for marketplace lending. Some investors, like Foundation Capital’s Charles Moldow, are betting on the market, between cannibalization and traditional banks moving into marketplace lending themselves, can grow to be a trillion dollars.

It’s not just marketplace lenders taking aim at banks. Traditional ecommerce players want in, too. Amazon is offering loans to handpicked sellers on goods on its ecommerce platform.

Like marketplace lending, ecommerce firms entering financial services isnt’ just happening in the US: PayPal’s Working Capital loans for small businesses has lent more than $1 billion to over 60,000 small businesses in the U.S., U.K. and Australia. Alibaba, the giant Chinese ecommerce platform, launched a money market fund for sellers to store their working capital. Within just 10 months, the fund, called Yu’e Bao had more than $90 billion in short term capital. That’s money that used to be kept in banks.

On the heels of Alibaba’s success in money markets, Chinese search engine Baidu appears ready to launch its own banking solution. Looking to avoid some of the regulatory commotion around Alibaba’s own financial service offering, Baidu intends to partner with Citic, the 7th largest Chinese bank with 600 physical locations.

While Google got out of the direct lending business to its advertisers, it is now running a pilot with Lending Club. The marketplace lender is offering advertisers on Google a loan to fund their AdWords campaigns.

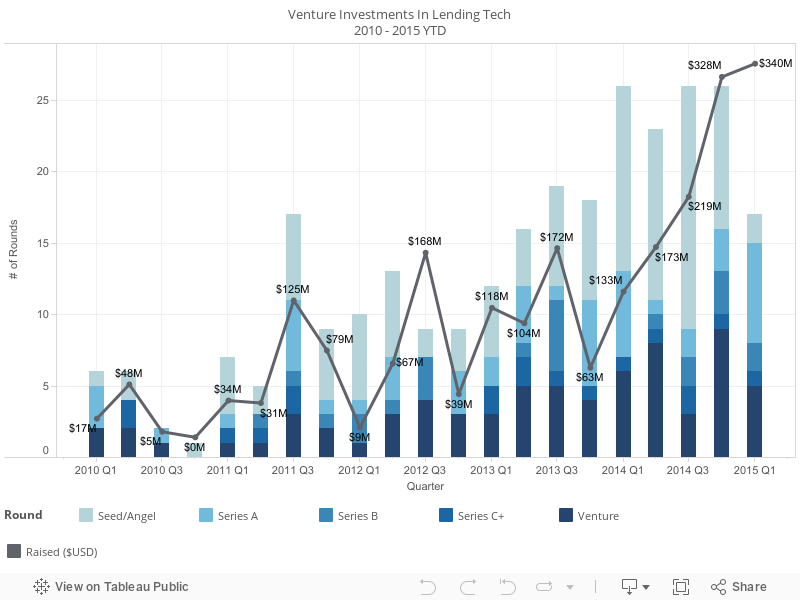

The nature of banking is changing and therefore, the players leading the charge are rearranging themselves. [x_pullquote cite=”TechCrunch” type=”right”]This year, over $11 billion has been invested in financial technology services companies. That’s up over $5 billion from the previous year, and the highest amount invested into financial services technology companies in the past five years[/x_pullquote]Pureplay lenders are filling an important role and ecommerce platforms have found a way to offer financing to some of their best customers. As this plays out, there are more companies popping up to help banks compete. Firms like LendKey provide banks with the tools, technology, and process optimization employed by nimble tech startups. More companies keep launching to help make the banking sector more competitive to the demands placed on them by consumers who are demanding the same speed, transparency, and service commonplace in other industries disrupted by technology.

This opportunity hasn’t been lost on investors, who are pouring money into alternative financing businesses. Lending Club and OnDeck both had well-received IPOs that gave the companies billion dollar marketcaps.

In 2015, there’s been hundreds of millions of dollars invested into alternative lenders. Just this week, alt lender Earnest announced a round of $275 million (equity and debt).

Regulation and branding will assure that banks aren’t going away but it’s getting more complicated to compete in core banking services. Direct competitors are emerging to challenge banks head on while others, like ecommerce players, are indirectly competing indirectly with them. Through general growth, partnerships, and some disruption, the banking industry is quickly evolving.

[x_author title=”About the Author”]

Every week at Tradestreaming, we’re tracking and analyzing the top trends impacting the finance industry. The following is a list of important things going on we think are worth paying attention to. For more in depth trendfollowing, subscribe to Tradestreaming’s weekly newsletter (published every Sunday).

1. Computers vs. Humans: Who wins the investment game? (Tradestreaming)

Do humans have an innate ability to pick winning stocks or should we turn everything over to the machines. A frank conversation with 2 experts moderated by Tradestreaming’s managing editor, Zack Miller and hosted on Dealbreaker.

2. A Future Where Virtual Reality and Finance Converge (Finance Magnates)

In this week’s Fintech Spotlight, Finance Magnates delves into how virtual reality could become a big data tool of the future in the finance industry.

3. The Next Fintech Boom: Resource Maximization (Bank Innovation)

Former Thomson Reuters CEO, Tom Glocer predicts fintech startups to begin squeezing more out of the financial system. “Think of all the underutilized financial resources out there — credit lines, savings, advisory, illiquid assets. All are ripe for maximization.”

4. Why Every Financial Institution Needs a Digital Champion Now (The Financial Brand)

Is anyone spearheading your organization’s digital strategy? Here’s what banks and credit unions should look for when creating this new role.

5. Robo-Advisors Squeeze Advisor Profits, Not Fees (Michael Kitces)

Michael Kitces with a thoughtful analysis of the robo-advisor trend and how it’s impacting the AUM fees investors pay (it’s not what you think it is). While fees don’t seem to be dropping, profit margins are indeed getting squeezed. Worth a read.

Yodlee’s been aggregating financial information and data for 11 years now, powering some of our favorite financial apps.![]()

Now, the firm is getting aggressive about enabling the next generation of fintech apps and platforms.

Chief Strategy Officer, Joe Polverari joins me on Tradestreaming Radio to discuss Yodlee’s new incubator/accelerator program and the resources the firm is committing to financial services startups.

Continue reading “Powering the next generation of financial apps — with Yodlee’s Joe Polverari”

Been talking a lot to entrepreneurs in the space. I get a chance to hear their perspectives on their financial backers, investors with an eye to the future of financial services.

Here’s the beginning of a list of some of the best VCs in fintech. Who do you think belongs on there?