Riskalyze works with investment advisors on assessing their clients’ true tolerance for risk and aligning their portfolios appropriately. The technology platform works with thousands of advisors to help manage over $120 billion in assets — at its core is its proprietary measure of risk, the Risk Number.

Riskalyze founder and CEO, Aaron Klein joins Tradestreaming to talk about how his firm’s approach to helping advisors understand risk better is changing the way they manage to their clients’ short- and long-term goals.

Keeping clients invested for the long run, and not allowing short-term risk to sabotage their performance.

There have basically been three waves of advice. The first wave was “my mutual fund is better than that guy’s mutual fund.” The second wave was “well, we’ve established my mutual fund isn’t better, but instead of talking performance, let’s focus on your long term financial goals instead.”

We think the third wave is risk-first. If we can align a client with the portfolio that fits their Risk Number, we can empower that human to give themselves the permission to ignore short-term risk, stay invested for the long term and actually achieve those long term financial goals.

A team of academics just went through our methodology and data, and what they found was fascinating. 52% of investors aged 20-29 don’t fit their stereotype of being aggressive. This is the client who is emotional and upset when markets are dropping because they have too much risk. Meanwhile, 53% of investors aged 70-79 don’t fit their stereotype of being conservative. This is the client who is frustrated that they aren’t getting the returns they want when markets are going up.

It turns out, people are individuals. They have Risk Numbers. And we ignore their Risk Numbers as a part of the investing equation at our own peril.

First, they’d start with stereotypical risk capacity. Young, aggressive. Old, conservative. Then they’d ask some nonsensical subjective questions like “do you get a thrill out of investing” and nudge the client to the right or left a little bit with each question. Well, guess what? People got a real thrill out of investing in 2013 and didn’t get quite as big of a thrill in 2008. That’s not risk tolerance — it’s market outlook.

They’d take that combination of stereotype and market outlook and toss the client into a buckets like conservative, moderate or aggressive. Then they’d match them with a portfolio carrying the same label by an asset manager who means different things by those words. This is the equivalent of me sitting down with my architect and contractor and deciding I want a “moderately conservative hallway leading to my moderately aggressive bedroom.” We haven’t decided anything. The Risk Number puts the feet and inches into this industry.

The Risk Number is a quantitative, objective measurement of how much risk clients want. Advisors will often come aboard and say “wow, my clients seem to want more/less risk than I think they should have.” Well, great. That’s why they’re paying you to be their advisor — to lead them to the right decision. But at least now you know what they want, and you can build a portfolio that aligns with what they want, and if you believe they’re off base, show them why they should instead take the amount of risk they need. That creates “fearless investors” — and that’s what we need if investors are going to achieve their long term goals in the face of their human instinct to react to short-term risk.

The Risk Number is a quantitative, objective measurement of how much risk clients want. Advisors will often come aboard and say “wow, my clients seem to want more/less risk than I think they should have.” Well, great. That’s why they’re paying you to be their advisor — to lead them to the right decision. But at least now you know what they want, and you can build a portfolio that aligns with what they want, and if you believe they’re off base, show them why they should instead take the amount of risk they need. That creates “fearless investors” — and that’s what we need if investors are going to achieve their long term goals in the face of their human instinct to react to short-term risk.

Well, if it’s a prospective client, the advisor can often demonstrate to the client that they have way more risk than they realize or want. That’s a powerful tool for acquiring clients. And for existing clients, it’s a way to “get real” and drive alignment between the risk the client has, wants and needs. As we say, “show prospects they’re invested wrong, prove to clients they’re invested right.”

One of our advisors captured his own Risk Number. He was a 52. Plugged in his own portfolio and it was a 51. (He rightfully felt pretty proud of that!) Then he plugged in his client portfolios which spanned from 45 to 65. Then he started capturing client Risk Numbers and they spanned from the 20s to the 80s.

It didn’t take him long to see the pattern. He was really good at figuring out which clients were more conservative than his 52, and which ones were more aggressive than his 52. But he was anchoring them to HIS Risk Number. He said “now I know why my conservative clients still feel scared and my aggressive clients still feel frustrated.” He was able to tell them he’s using new technology to measure their risk with greater precision, and now he’s got each of his clients aligned to themselves.

We have 90 employees (we call them Riskalyzers) serving thousands of advisors managing over $121 billion in assets on the platform. We’re thrilled to be working with advisors and wealth management enterprises across the industry to help them drive risk alignment, and at the same time, drive huge efficiency in their business. Our Autopilot digital advice platform is taking the Riskalyze process and flipping it to be client-driven, often advisor-assisted. And our Compliance Cloud platform is helping enterprises sift through their books of business for compliance issues.

Everything feels different, but the reality is, everything is the same. Here’s what I mean: the press can’t help but print any story that has the word “robo” in the headline. I swear, one day we’re going to have an article about Merrill Lynch allowing their advisors to use iPads and the headline will say “Robo tablets arrive at the thundering herd.”

Here’s the truth: you still have advice businesses, and you have self-directed businesses. Wealthfront and Betterment are self-directed robos. They’re just self-directed brokerage accounts with way better user interface. Meanwhile, Personal Capital and Vanguard Advisor Services are advice businesses, not robos. They’ve hired armies of CFPs and leverage great technology to support a high client-to-advisor ratio.

In five years, there will be a plethora of digital advice platforms, because the diversity of thousands of advisory business models and approaches won’t go away, and our different advisor-facing technology needs to become more client-facing. We’re going to offer Autopilot there, but we’re also going to work with partners because our mission isn’t “bringing the world’s assets onto our digital advice platform,” it’s “aligning the world’s investments with each investor’s Risk Number.” And we’re not going to rest until we achieve that because it changes the world for the better.

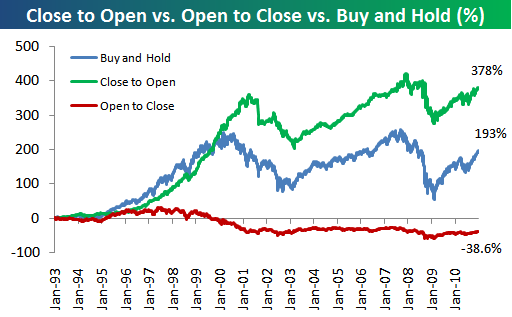

Investors seem to be more focused on the short term than ever.

You can credit hedge funds and institutional investors having to report performance on a monthly basis. CNBC’s 24/7 coverage of financial news doesn’t help, either.

However we got here, many analysts are calling for a return to longer term frameworks for investing — for investors and managers that run the companies they invest in.

Finance professor, Al Rappaport has been analyzing shareholder value since his first paper on the subject in 1965.

His new book, Saving Capitalism from Short Termism: How to Build Long-Term Value and Take Back Our Financial Future is a clarion call to break out of our current myopia and find a way to focus on long term value.

Rappaport joins us on Tradestreaming Radio today.

Al is a professor emeritus at the Kellogg School of Management where he taught for many years. He’s the author of numerous other books and papers, many with a focus on maximizing shareholder value.

Al is a professor emeritus at the Kellogg School of Management where he taught for many years. He’s the author of numerous other books and papers, many with a focus on maximizing shareholder value.

Photo credit: eblaser / VisualHunt / CC BY

This event was already held. Check out this event’s presentation, Building an investment advisory business from the ground up.

|

|||||||||||||||||||

From the ground up: How to build a successful money management firm |

|||||||||||||||||||

|

The hedge fund industry certainly took a drubbing in the bleak market years which were 2007 – 2008. But, they’re back and they’re back on the heels of good performance and inflows in 2010. Credit Suisse released its 2010 Hedge Fund Industry Review (.pdf) today.

Few highlights:

Check out the whole report here.