Small bank, big moves: Six Gen AI use cases that move the needle for small banks (and three that don’t)

- In our new two-part special series we will discuss how small banks and FIs can close the gap and compete with billion-dollar AI investments from mega-banks through strategic Gen AI implementation.

- Dive into six use cases from fraud detection to marketing and learn which AI applications deliver maximum ROI and which ones small banks should avoid.

Doing more with less is the small bank mantra but burdened with legacy tech and consumers’ preference for digital experiences, small banks and FIs have their work cut out for them.

Especially when it comes to Gen AI.

On the one hand, the potential Gen AI offers for increasing competitiveness, CX, and efficiency demands action, on the other, are the constraints of time, money, and resources, bogging down any meaningful discussion on AI strategy.

But small banks must find a way to break free of these chains of legacy and size, especially when the biggest players are making billion dollar investments in Gen AI and capturing thousands in the talent pool.

This article is the first in a series of two focused on how small banks can capture the competitive advantage of Gen AI. In this edition, we will discuss what use cases may supercharge small banks’ efficiency and customer experience and which use cases aren’t likely worth the investment for firms under $10 billion.

Use cases that work

With limited resource availability, small banks and FIs need to identify areas where they can get the most bank for their buck.

Six use cases emerge here, according to Ryan Lockard, Principal at Deloitte:

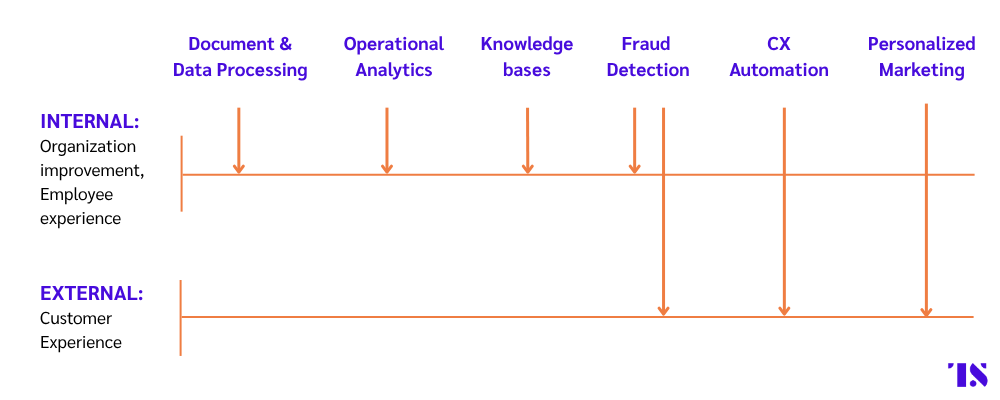

i) Fraud Detection: Bad actors are already using Gen AI to game financial systems for their gain. Criminals were able to defraud Americans out of $21 million between 2021 and 2024 using voice cloning technology the efficacy of which has been significantly improved by modern LLMs. Most big organizations are fighting this fire with fire, and using Gen AI tools to identify new types of fraud tactics as well as improve their fraud detection systems. Small banks can use these same systems to adopt real-time fraud monitoring with automated alerts to stay ahead of criminal activity.

ii) Customer Service Automation: Bank of America is about to enhance its award-winning digital assistant Erica with Gen AI. Small banks and FIs can learn from this playbook, and integrate Gen AI technology in their digital customer service agents to drive better response times and enable their staff to focus on higher-value processes.

iii) Personalized Marketing: Smaller FIs often operate with a limited marketing budget and team. Here, Gen AI tools can help better audience analytics by improving segmentation and targeting as well as help FIs create more with less through content generation.

For example, Duke University Federal Credit Union (DUFCU) recently integrated Vertice AI’s copywriting tool called COMPOSE. “The marketing team can prioritize delivering high-quality content that drives new member growth. COMPOSE is equipping us to elevate our standards of excellence, while streamlining our efforts, ensuring our acquisition campaigns are highly personalized, on-brand and efficient,” said DUFCU’s Director of Marketing Jennifer Sider.

Industry-specific tools offered by financial technology providers like Vertice are a critical differentiator here. They are trained to be compliant with financial services regulations, and can keep up with evolving regulations with relatively low-lift from FIs, and also learn from internal material to ensure messaging is in-line with the tone of the firm.

iv) Document and data processing: There is a misunderstanding in the market that just because data is available, lenders and FIs have the capabilities in place to be able to utilize it effectively. 61% of lenders report being overwhelmed by the volume of data available. Gen AI can prove to be of significant value here.

For example, the $2.5 billion, Kentucky-based Commonwealth Credit Union integrated a tool by Zest AI called LuLu Pulse, which uses Gen AI to consolidate multiple data sources like NCUA Call Reports, HMDA, and economic data, allowing the firm to gain insight into how their products and services compare to their peers.

Additionally, Gen AI-driven KYC processing can also accelerate onboarding, improving customer experience and minimizing the chance of errors.

v) Operational Analytics: Small FIs can also use Gen AI to take a closer look at the health and efficiency inside their organization. Gen AI powered operational analytics can help firms identify process bottlenecks and improve resource allocation, allowing these firms to build as much efficiency into their lean workforce as possible.

vi) Knowledge bases: Access to Gen AI-powered knowledge bases can prove to be useful for small teams, offering them quick access to information around internal policies, simplifying employees’ workflow. Banks like Citizens are already implementing such tools allowing everyone in the management chain to access information about topics like employee benefits.

Use cases that DON’T work

Given limited resources and time, small FIs need to make sure that their approach to Gen AI integrations focuses on use cases that are meaningful.

Highly complex and infrequent: Processes like complex lending decisions, where human expertise and understanding play a big role, aren’t suitable for Gen AI implementations. Low-volume, high-complexity tasks are also unlikely to yield ROI for small FIs, according to Lockard.

Poor data quality: Firms must also keep in mind that Gen AI’s output is only as good as its data. So any use cases that hinge on poorly structured legacy data aren’t a good fit for Gen AI implementation, shares Lockard. When assessing whether a use case will benefit from Gen AI implementation look for well-labelled and annotated because it allows Gen AI models to learn more quickly and produce better outcomes.

Code generation: Additionally, while people are getting excited about Gen AI’s ability to write code, only firms with in-house development teams may be able to fully leverage such features. Without in-house technical expertise to properly vet, customize, and maintain AI-generated code, organizations may face security risks, integration failures, and compliance issues that far outweigh any potential benefits.

Gen AI use case suitability checklist:

- Does the use case occur frequently enough to justify investment?

- Is there a clear goal and KPI that would help measure the impact of Gen AI integration?

- Would the lack of human intervention in this use case severely negatively impact results?

- What mechanisms are in place to take corrective action in case something goes wrong?

- Who will be held accountable for mishaps?

- What regulations impact Gen AI usage in this use case and is there tolerance for regulatory action against the organization?

- Is the underlying data infrastructure and data ready for Gen AI integration?

Gen AI implementation holds massive potential for those small FIs that can rally their C-suite and employees to adopt the tech.

“By automating manual tasks, Gen AI drives operational efficiency, reducing both costs and error rates. It also transforms the customer experience, delivering personalized, always-on service that can rival what the largest institutions offer. But perhaps most importantly, cloud-based AI solutions empower small banks to bring new products and services to market at a speed closer to that of Universal Banks and GSIBs, closing the innovation gap and leveling the playing field.”

— Ryan Lockard, Principal at DeloitteIdentification of the right use cases is the first step in building a Gen AI strategy, stay tuned for the second part of our series to learn how to get started once the feasibility studies are over.

We will cover:

– Implementation strategies

– Change management

– Role of technology providers

– Talent acquisition