Unpacking Brigit’s journey to $100 million in revenue

- PFM app Brigit surpassed $100 million in revenue in 2023. What are the key drivers behind this milestone?

- CEO Zuben Mathews credits the revenue increase to three main factors: effective marketing, strategic product launches, and their cash flow technology.

Brigit, the personal finance management [PFM] app, revealed last month that it achieved a significant milestone, surpassing $100 million in revenue last year. The fintech is backed by NBA [The National Basketball Association] star Kevin Durant’s Thirty Five Ventures and Lightspeed Venture Partners, among other investors.

In addition to providing various financial wellness tools, Brigit’s core value proposition revolves around cash advances and other protections against overdraft fees.

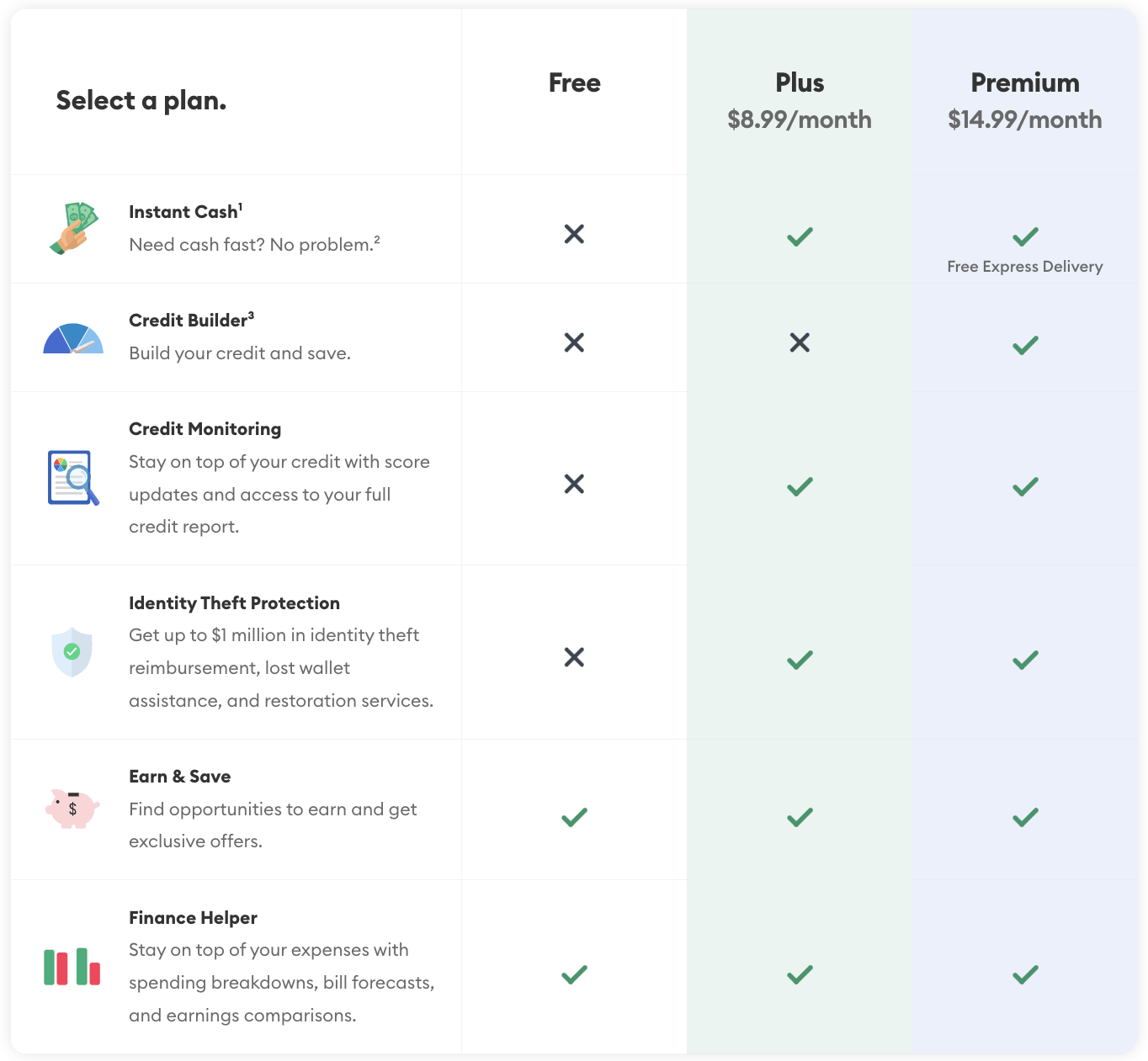

How Brigit works

The app operates by linking directly to users’ bank accounts, where it evaluates their income sources and spending habits. Leveraging this information, it offers short-term cash advances aligned with their earnings, without accruing any interest charges. Repayment is made as the app automatically deducts the borrowed amount from the user’s bank account usually on their next payday.

But there are no free lunches. To access this feature users are required to opt into a monthly subscription plan – Plus or Premium. Upon approval for Instant Cash based on certain factors like spending and income, users can anticipate receiving deposits ranging from $50 to $250 in their linked bank account within 2-3 business days. Customers who want their money quicker can pay an express delivery fee. The express delivery is free with their new Premium subscription, which also exclusively includes the Credit Builder product.

By tracking users’ transactions and spending habits, the app also provides alerts regarding upcoming bills and assesses users’ financial capacity to meet their expenses. If there’s going to be a shortfall, Brigit, with a Plus and Premium membership, will automatically advance up to $250 into the user’s account before overdraft fees kick in, potentially saving users from penalty charges.

The inception and the key ingredient

Currently staffed with 80 employees, Brigit was founded in 2017 to challenge overdraft fees imposed by major banks, according to CEO Zuben Mathews.