Gen AI can prove to be a powerful tool for institutions that struggle to keep up with larger institutions but don’t possess the resources, and time to match their throughput.

Today’s micro case studies dive into how two CUs are improving their lending decision making and marketing efforts through incorporating Gen AI tools in their workflows.

1) How Commonwealth Credit Union is improving strategic decision-making in lending through Gen AI

When it comes to analytics, 61% of lenders find the large swathes of customer and lending data available in the market overwhelming and 73% report that their limited ability to leverage data impacts their competitiveness, according to research.

This points to a significant gap between data sources and FIs’ ability to extract useful insights. Lenders that can understand their positioning compared to their peers in factors like delinquency, chargeoffs, and interest rates are better able to provide competitive products.

Commonwealth Credit Union is particularly aware of how this impacts the firm’s ability to compete. “Our competition isn’t waiting weeks for data. They’re making decisions today on data that they got today,” said Jaynel Christensen, EVP, at Commonwealth Credit Union.

The backstory

Recently, the $2.5 billion, Kentucky-based CU decided to fill in this gap by integrating a tool by Zest AI called LuLu Pulse, which uses Gen AI to consolidate multiple data sources like NCUA Call Reports, HMDA, and economic data. This ultimately allows lenders to gain insight into how their products and services compare to their peers by querying the platform.

The recent integration of LuLu Pulse builds on the Commonwealth’s long standing partnership with Zest AI, through which the CU has also utilized underwriting resources and fraud protection tech.

Managing money alone is hard enough but when two people and their respective money stories get married, things can get a lot more complicated.

This is the problem Plenty’s CEO and cofounder Emily Luk set out to solve after she got engaged. She noticed a lack of financial tools for couples and decided to build Plenty, a financial tool that helps couples manage their finances in one place.

Plenty allows couples to track shared and individual finances, as well as save and invest towards shared and personal goals.

“There was one thing that was really different from how we thought about things as a generation. There wasn’t really an expectation that one person works, one person manages all the money. No, we’re both working. But it was so hard even to do the simplest thing – we both use a credit card, and I want both of us to know what we’re spending on it,” said Luk.

Emily Luk, CEO, Plenty

This is how Emily Luk built a finch that has seen 8x growth in users since December 2024.

From fintech employee to fintech founder

Luk is no stranger to the financial industry. She was one of the first 20 members of Stripe’s growth team and in her three years at the company ran initiatives like pricing merchants across the different geographies and forecasting for all the firm’s software products.

“Stripe really was one of the first companies to take a part of the financial industry and really digitize it. I think that was one of the things that I saw: for so long, payments was such a legacy business, and yet they were able to modernize it,” Luk said. After Stripe, Luk joined Even which was later acquired by Walmart for its fintech venture, One. At Even, Luk was the VP of Strategy and Operations running the company’s goal setting efforts as well as fundraising and investor relations. “Even was really focused on helping people living paycheck to paycheck, reach a point of stability. What was really exciting there is we ended up building a product that reached a million and a half people. Through that, I had a chance to see how big of an impact we could make making software,” she said.

While the hard and soft skills that Luk built in her time at Stripe and Even have a clear carry over effect to Plenty, her connections within the industry have had an effect too.

The following are all investors in Plenty:

Adam Nash, ex-CEO of Wealthfront,

Brian Delahunty, Head of Engineering at Anthropic

Mark Goines ex-SVP at Intuit and ex-VP at Charles Schwab are all investors in Plenty.

Kevin Durant, all-star professional basketball player

Fintechs and challenger banks have leveraged channels like TikTok, Instagram, and YouTube much more effectively and frequently than traditional banks.

To put this in perspective, JPMC, Bank of America, Wells Fargo, and US Bank all have a TikTok channel and official account on the platform but their pages have no content on them whatsoever. Only Citi and Capital One seem to have an active presence and strategy for this channel.

The absence of a dynamic and evolving social media strategy directly impacts how these banks connect with younger audiences. It’s a missed opportunity to build trust, recognition, and loyalty.

So what’s keeping the biggest financial brands in America from acting and building strategies for channels like TikTok?

A big reason for it may be the newness of it all, according to Kelvin Chen, Head of Policy at the Consumer Bankers Association, a trade association representing the retail banking industry. “It’s a new platform, and by virtue of that, it’s a little scary. The influencers that you’re working with all have relatively limited track histories,” he said.

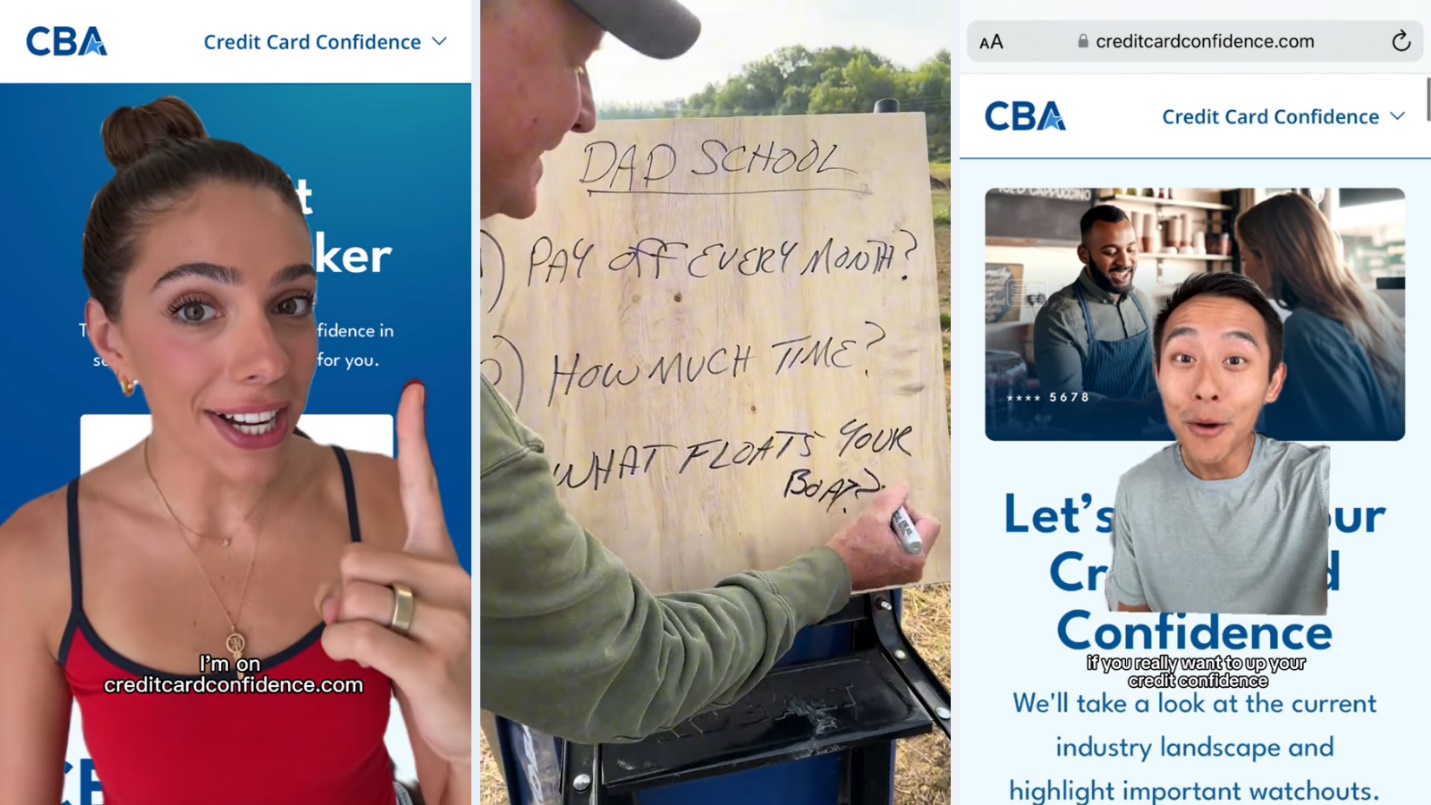

Despite the novelty, the CBA itself recently dove in headfirst and partnered with influencers for its Credit Card Confidence campaign. The campaign’s primary objective is to help consumers understand credit cards and their relationship with them better through answering three questions on the campaign website. Through this financial literacy campaign, the CBA aims to counteract some of the “bad rep” that credit cards have been getting in the media lately, according to Chen.

To maximize the campaign’s reach, the CBA has partnered with a number of influencers on TikTok and is using their videos to summarize the salient points of the campaign’s messaging and to redirect viewers to the campaign website. “Banks have sent 600 [million] pieces of mail a month to people’s homes, and that still isn’t hitting. Is there a different modality that might work?” said Chen.

The campaign and CBA’s process serve as a case in point for FIs that want to build a presence on channels like TikTok without rocking the regulatory boat.

Beyond this goal, the CBA is also hoping to get access to data and build a data team that would allow different parts of the organization like regulatory lawyers, lobbyists, and communicators to “to speak as one”, Chen added. Through the campaign the firm is also workshopping how to take insights from research and turn it into short form messaging. “The goal is to be able to take complex data driven messaging that’s heavily researched and turn it into a simple TikTok message, but to make sure that every word in there is airtight,” he said.

Building content that is trustworthy

The Credit Card Confidence campaign draws heavily from behavioral economics principles, and the questions on the campaign’s website have been green lit by experts in the government, consumer advocacy space, and the banks that the organization represents, says Chen. Unconventionally, the campaign doesn’t endorse or mention any specific credit card products or brands. The downside to this is obvious: beyond the advice, customers don’t have a direct and clear link to products that would suit their particular lifestyle and preferences.

But compromising on this last bit of experience allows the campaign to build a sense of trust and authenticity that feels untouched by advertising motives. It allows the advice to be truly product agnostic which can be important in an industry that has a “very heavy economy of lead generation”, said Chen.

While brainstorming the campaign, one of Chen’s mentors and an expert in the credit card industry said “I don’t know that anyone’s doing this well, because it’s all lead gen. Everyone has a particular set of products that they’re pushing consumers towards, and so, even if they’re well intentioned, it’s a limited set of products that they’re working with.”

Building content that is engaging

When it came to who to work with for the amplification on TikTok, the CBA chose influencers like John Liang (2.4 million followers) and Taylor Price (1.1 million followers), both of whom provide finance tips on the channel. Another influencer that the CBA has partnered with is Bo Petterson (3.7 million followers) who self-describes as a “regular dad teaching you what I taught my kids & fighting for my daughter’s cure”.

In his video for the CBA, Petterson can be seen standing in the middle of a field with his horses, summarizing the content on the campaign website and writing down the salient points on a board. Price’s version uses a popular short-form video format “Get Ready With Me (GRWM)” which usually involves the influencer talking while doing their makeup.

“There was an old-fashioned brand exercise where we asked if this is people’s first impression of us, what’s the feeling we want them to have about the CBA? We didn’t want to make it seem like we’re the old man in the shirt that’s too tight in the nightclub. At the end of the day, we really like Bo for instance – because we’re the old people in pleated pants, just trying to tell you what we know about life in a humble way,” Chen said.

All of the TikToks in the campaign clearly show that the video is made in partnership with the CBA, come with disclosures, and are intentionally less than minute long, he added.

Snapshots from the campaign’s TikToks, Source: CBA

How to measure success

The CBA is currently amplifying some of its videos with paid marketing, and its choice of social media platform depends upon the engagement analytics tools that come with the website to track the content’s performance. “We’re pulling in data, and we’re able to look at reshares, comments, and likes, and then see what’s working and what’s not,” he said.

At first Chen thought that views would be the biggest indicator of success, but as the campaign is progressing, Chen feels that some other metrics are more indicative of consumer opinion, especially given that the campaign isn’t built around tracking conversions to a particular product. So far, Chen reports that the campaign is nearing 10 million views, despite only being halfway through its run time. Metrics like bookmarks, reshares, and comments better express how much customers trust the content they are watching. “The thing that I love the most is that we have 700 plus comments and like, 3000 plus reshares… in my mind, there’s no better validation than someone saying, hey, I saw this and I thought this was interesting. I’m going to send it to my mom or send it to my friend,” he said.

Social media channels like TikTok allow brands to actually see who is willing to promote their products and messaging, a thing that Net Promoter Scores only have a hypothetical estimation on. For institutions that aren’t on these channels, one issue is the possibility of their messaging getting drowned out in the sea of content.

Earlier this year U.S. Bank’s Head of Behavioral Science, Julie O’Brien said “… we can’t influence what people are exposed to, outside of our own institution. And I think that’s something that we have to think about. We’re only one voice out of many voices, that can be very powerful, in comparison.”

But the noise of social media isn’t a reason for FIs to avoid platforms like TikTok. It’s exactly why they should join in and build their own marching bands.

Sidebar: The fintech approach to influencer marketing

The sidebar is a member-exclusive section where we discuss stories that are tangential to the main story above. In this sidebar we will discuss some recent campaigns by fintechs that relied on influencer marketing and whether they achieved their intended purpose.

In 2023, Wise launched a rebrand that has the potential to make it into design school curricula. With its citrusy green, bold typography, and painterly approach to 3D visuals, the Wise brand today is unforgettable without being overwhelming.

In today’s story, we do a deep dive into the impetus behind this rebrand, its scope, how it was executed, and the results the brand has seen since the unveiling of the splashy new look last year.

Problem statement: Reflecting growth and maintaining recognition

The shedding of the word “Transfer” in Wise’s name came before the new look. The company was slowly building towards its new identity driven by its growth in terms of geographies it served, as well as the products it offered. Wise was no longer just about sending money – it had products that enabled customers to hold and spend money and it touched more people now than ever before.

The challenge, however, was making sure that the firm does not lose the trust customers had with the company and its brand recognition as it went through its metamorphosis, according to the firm’s CMO Cian Weeresinghe.

To ensure customers moved with the firm, the team at Wise decided to march as one. “This [maintaining brand recognition] was no easy feat, and required intense coordination and collaboration across multiple teams and channels including paid marketing, PR, CRM, brand systems, product discovery, organic social, and customer service,” said Ciam.

The Wise rebrand has been so successful because every part of the business feels like a vignette out of the same story.

The remit: A redesign with expanse and depth

Wise feels different since its rebrand. It feels alive and exciting. Chasing ephemeral feelings is difficult but if there is anything that can make you feel closer to a brand and view it with renewed excitement, it’s design.

And Wise’s new look was all encompassing. It’s hard to remember what Wise looked like before because the pieces today fit so well together. The same cannot be said for rebrands like that of Twitter, where the X and flat blacks only evoke nostalgia for better days.

Here is what Wise changed in the rebrand and how the firm thought about each piece:

a) Color Palette: The most noticeable change for Wise was perhaps the shift in its primary colors. The firm went from a safe blue to an energetic and electric green. “Wise doesn’t think of itself as a bank. It doesn’t act like a bank. The new green color represented a chance to make that stand again against what is a sea of sameness when it comes to other financial services brands,” said the firm’s VP of Brand Strategy, Iona Carter.

Carter also shared that the green helped with evocation by representing money and progress. Another important consideration for the wider color palette was accessibility. Testing and consumer feedback played an important role here in ensuring that the new look met both WCAG guidelines as well as APAC color standards.

b) Visual Elements: Some of the best global brand identities and designs, like Apple, use 3D elements. Wise was one of the first brands to really own the 3D direction and is still one of the few brands in the financial services industry, particularly, to do so.

The Wise homepage today is dominated by a green-blue 3D globe that is orbited by currencies from various countries. The connection to Wise’s global nature and financial focus is clear from the outset. It was this globe that inspired the adoption of the 3D assets into other areas of the Wise website, says Carter.

The impetus for going in the 3D direction was the same as that for choosing green: Wise wanted to be distinctive and it wasn’t afraid to lean in. “2D illustrations are pretty rote at this point within brand identity systems,” said Carter.

3D design elements are more powerful than some may think. The gaming industry entered a new era when video games stopped being 2D and built immersive worlds by playing with light, environment, and movement. 3D visual elements give a sense of depth and realism, driving deeper engagement and connection.

For 3D illustrations texture is an important consideration, and Wise made what the firm calls “graphic tapestries” inspired by bank notes and visual elements from historical places, to come up with a painterly effect that gives these elements a rich, plush, and smooth feel.

“There’s enough thinking and theory now, at least in academic circles, around the importance of really distinctive assets for a brand,” said Carter.

c) Photography: Photographs help with feeling familiarity and grounding the design in the real world. For the rebrand, Wise wanted the photograph to emulate the dynamism that its other assets had.

“It’s challenging as a brand with a global reach to feel local, but also communicate globally. We felt photography was one element that we could really lean into that would enable us to do that,” said Carter.

The new photography came after careful art direction, and engenders a sense of movement, candid moments that represent real people, real emotions, and real moments from people’s lives.

The process: Keeping an eye on the ball and finding the right design partners

The Wise rebrand is successful not just because of what the firm accomplished, but also because of how it was done. From internal championing of the rebrand, deployment, to finding the right design company to work with, the processes of this rebrand are integral to the firm’s success with the project.

a) Deployment: Given that the digital touchpoints were now going to contain graphic-heavy assets, the team thought about how these designs will be implemented and deployed in customers’ experiences from day one, according to Carter.

“We were thinking about how what we built was going to be compatible with the Wise app, how it would work across desktop environments as well as how we could build a system that was ultimately simple but very scalable. We have a whole team now that just owns this remit called, ‘Brand Systems’,” said Carter.

She also shared that the firm has invested more heavily in building this team since the rebrand, with Brand Systems having grown considerably since the rebrand first rolled out.

b) Internal champions: With a wide ranging rebrand like this that impacts both high level things like color palette but also microinteractions, it’s important to keep reminding teams why they are doing what they are doing to act as a homing signal.

“Its an often overlooked job for any team that is spearheading a rebrand internally. [You need a] continual drum beat, that reminds people why we are doing this and contextualizing it,” Carter added.

c) Find the right partner: For the rebrand, Wise worked with Ragged Edge, a branding agency based in London, which has also worked with brands like Papier and Monzo. “We worked extremely closely with the Ragged Edge team, at every stage of the process, from ideation all the way through to how is this going to roll out in the product,” Carter shared.

Once the rebrand was done, Wise decided to continue its relationship with Ragged Edge, deciding that brand management, evolution, and design is a continuous process:

“The team intentionally opted to keep them in a retainer capacity. Because, the work of a rebrand, and in some ways, is never done. We’ve continued to work with them, albeit on a lower drum beat.”

The results are in

Not all rebrands reinvigorate excitement about the firm. Twitter’s rebrand to X actually led to its downloads dropping, as well as a 4% drop in active users. This is despite the fact that the firm was now attached to the most famous tech personality in the world, Elon Musk.

For Wise, however, the numbers tell a positive story. For the financial year of 2024, 48% of personal customers and 60% of business customers are using more than one Wise product in comparison to 36% and 55% respectively in 2023, according to the firm’s CMO Weeresinghe.

The firm’s overall growth also reflects the success of the rebrand, with the firm experiencing a 34% YOY growth in the first year (2022-2023) after the new identity’s launch and another 29% growth to 12.8 million active customers by the end of the financial year 2024.

The above graphic is created by Tearsheet using assets from the Wise website.

Sidebar: Branding makes perfect

Branding can be a powerful tool for communicating a firm’s core message, values, ethos, and personality to customers. And the more creatively a firm things about using assets and channels, the better.

Some time back the brand ran an interactive ad campaign called the “K-rated”. The ads had scannable pixelated images which curious customers would have to scan to get information of the product and access to deals. The whole campaign took inspiration from sex and porn and turned it into an interactive shopping experience. Klarna worked with the creative agency Thinkerbell on the campaign and Thinkerbell founder, Adam Ferrier told me that the idea was developed collaboratively by the two companies.

“Creating scarcity, or making something seem like it’s not easily available has the impact of people wanting to see it more. We used this psychological tool to make everyday objects seem ‘k-rated’, and could only be viewed via scanning the item via a QR code,” Ferrier said.

Another modality for brand and design heads to consider is sound. Think of sonic branding as a brand’s auditory handshake – it’s what ties the object (brand) to its attributes (convenient, trustworthy, etc.) in consumers’ minds.

“Sonic branding can be leveraged to build recall and association between brands and their campaigns and special products/services. Specifically in the financial services sector, sound branding can provide levels of assurance to the consumer surrounding the exchange of money or services,” said Austin Coates, Research & Insights Consultant at amp, a sonic branding agency.