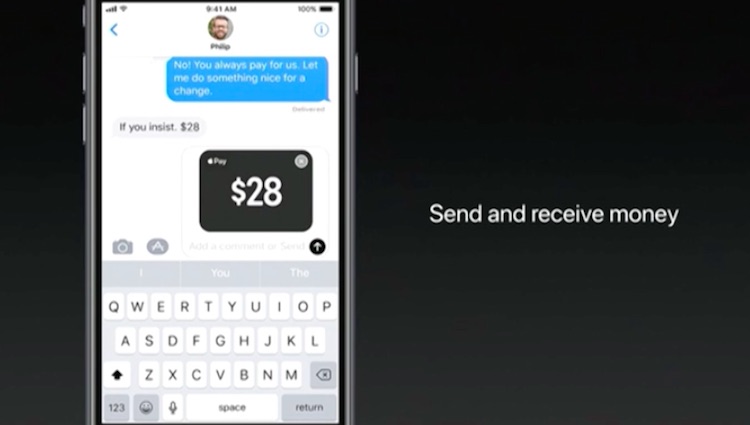

Posted on April 21, 2017April 21, 2017How Mastercard is applying lessons from Apple Pay to its plastic cards

Posted on February 10, 2017March 16, 2017On the road to voice payments, Google and Amazon pull ahead of Apple