Unpacking Brigit’s journey to $100 million in revenue

- PFM app Brigit surpassed $100 million in revenue in 2023. What are the key drivers behind this milestone?

- CEO Zuben Mathews credits the revenue increase to three main factors: effective marketing, strategic product launches, and their cash flow technology.

Brigit, the personal finance management [PFM] app, revealed last month that it achieved a significant milestone, surpassing $100 million in revenue last year. The fintech is backed by NBA [The National Basketball Association] star Kevin Durant’s Thirty Five Ventures and Lightspeed Venture Partners, among other investors.

In addition to providing various financial wellness tools, Brigit’s core value proposition revolves around cash advances and other protections against overdraft fees.

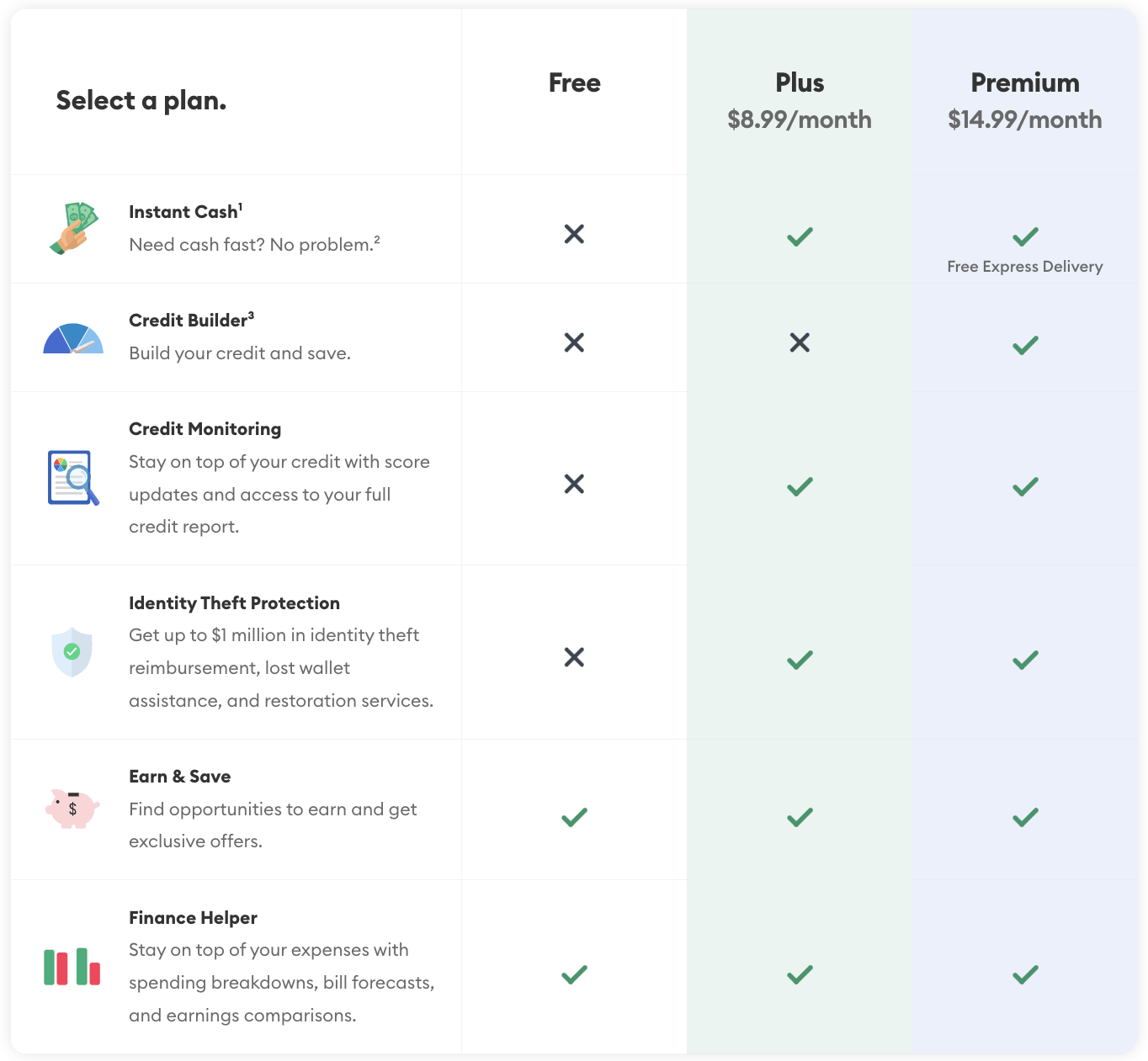

How Brigit works

The app operates by linking directly to users’ bank accounts, where it evaluates their income sources and spending habits. Leveraging this information, it offers short-term cash advances aligned with their earnings, without accruing any interest charges. Repayment is made as the app automatically deducts the borrowed amount from the user’s bank account usually on their next payday.

But there are no free lunches. To access this feature users are required to opt into a monthly subscription plan – Plus or Premium. Upon approval for Instant Cash based on certain factors like spending and income, users can anticipate receiving deposits ranging from $50 to $250 in their linked bank account within 2-3 business days. Customers who want their money quicker can pay an express delivery fee. The express delivery is free with their new Premium subscription, which also exclusively includes the Credit Builder product.

By tracking users’ transactions and spending habits, the app also provides alerts regarding upcoming bills and assesses users’ financial capacity to meet their expenses. If there’s going to be a shortfall, Brigit, with a Plus and Premium membership, will automatically advance up to $250 into the user’s account before overdraft fees kick in, potentially saving users from penalty charges.

The inception and the key ingredient

Currently staffed with 80 employees, Brigit was founded in 2017 to challenge overdraft fees imposed by major banks, according to CEO Zuben Mathews. US banks generate significant revenue from overdraft fees, pocketing over $7.7 billion in late fee revenue in 2022.

While a $35 overdraft fee may appear trivial to some, the compounding effect of these charges can be significant, particularly when incurred for each transaction during a negative balance. On average, an overdraft can dent a user’s finances by $68, with occurrences often multiplying within pay periods, burdening those reliant on each paycheck, said Mathews.

To date, Brigit claims to have provided $2.3 billion to its members and saved them $1 billion in bank fees. Despite navigating through uncertain economic landscapes in recent years, the company has also managed to surpass $100 million in revenue in 2023. It anticipates 50% revenue growth this year with an aim to sustain profitability.

According to Mathews, the revenue increase has largely been a function of three things:

1. Effective marketing: The firm has grown its paid member base via effective marketing.

2. Introducing products that complement existing products: The company introduced a higher subscription level, Brigit Premium, which includes the Credit Builder product. The Credit Builder is strategically introduced to integrate with and strengthen the current offerings in Brigit’s ecosystem.

Mathews explained that Credit Building, for instance, can unlock further opportunities within their marketplace, potentially leading to reduced insurance expenses for users with improved credit scores.

“Every new product or feature that we incorporate into our app aims to further our core mission and complements other products,” he said.

3. Cash flow technology: In addition, the company’s cash flow technology shines as the driving force behind this achievement.

The firm attributes much of its accomplishment to its technology-driven risk and collections platform, with machine learning and AI technologies at its core. The technology can analyze 7,500+ data points per user enabling the fintech to greenlight twice as many individuals as traditional lenders.

“Our model allows us to react more quickly than traditional lenders because cash flow data tells us what’s going on for this customer today rather than what happened 2-3 months ago from their credit reports,” said Mathews.

“This is a 100% automated process, resulting in strong unit economics,” he added.

Is the model sustainable?

Although the market hasn’t been particularly favorable for PFM apps marked by the shutdown of Intuit’s Mint, there’s been a larger conversation brewing about the viability of standalone PFM models. Mint’s demise was attributed to financial struggles but it also sparked debates about the sustainability of single-product approaches in the industry.

Brigit, however, seems to have found a winning formula with its multifaceted model. By offering short-term cash advances with overdraft fee protection in addition to other PFM services, the company is plotting a scalable revenue model to navigate through the changing economy.

Cash advances are anything but novel and are, in fact, a common offering, with neobanks such as Chime, Dave, and MoneyLion. While these digital banking platforms offer savings and checking accounts with a range of other products as part of their multi-product approach, Brigit has not transitioned into the digital banking space.

Unlike traditional lenders, Brigit’s business model is not reliant on the amount borrowed by its members, according to Mathews.

“As their [users] finances improve and they learn how to budget better, save more, and borrow less, it costs us less to serve them,” he said.

The fintech, however, is directly dependent on consumers’ dollars. Brigit generates most of its revenue through its monthly subscription model.

Regarding the firm’s strategy for increasing subscription conversions, Mathews explains that they emphasize showcasing the product’s value to users prior to subscription. For instance, they leverage their Cash Flow Engine to offer tailored money-saving recommendations and tips, along with personal finance content.

“It’s all actionable information that leads to high engagement. This means our users keep finding value in our products and convert to a paying membership,” Mathews said.

Unlike the higher interest rates charged by traditional payday lenders, cash advance apps seek a different revenue approach, relying on subscription fees and instant payment transfer charges. Though not explicitly labeled as interest, these fees can sometimes mirror the high costs typically associated with traditional loans, according to consumer advocates.

Frequently likened to the Earned Wage Access [EWA] model, cash advance apps share certain similarities with EWA, too.

The EWA terrain is undergoing evolution. Regulators are grappling with coming to terms with the fact that the EWA model exceeds existing regulatory boundaries and falls into a legal gray zone. EWA services provided by third parties may qualify as loans and will be subject to the state’s lending regulations. The decision to consider them as credit or advances essentially stems from the fact that the overall cost of using EWA products is comparable to that of predatory payday loans. This sentiment tracks concerns raised by consumer advocates regarding subscription and instant transfer fees charged by cash advance apps.

While Mathews recognizes that Brigit overlaps into the territory of EWA, it’s more akin to a Venn diagram where there are shared elements but also distinct differences. He emphasizes that the company does not fit squarely into that category.

“To say that we’re only focused on the earned wage product isn’t totally right,” Mathews added. “In that, we’re looking at how our products work together to improve our users’ overall financial wellness.”

According to him, the firm is engaging with regulators to understand regulatory provisions, while also monitoring potential changes that could impact their platform.

Brigit faced legal turbulence toward the end of last year though. The Federal Trade Commission [FTC] accused the company of misleading practices. Although Brigit denied the allegations, the fintech agreed to settle the case for $18 million.